7 September 2021

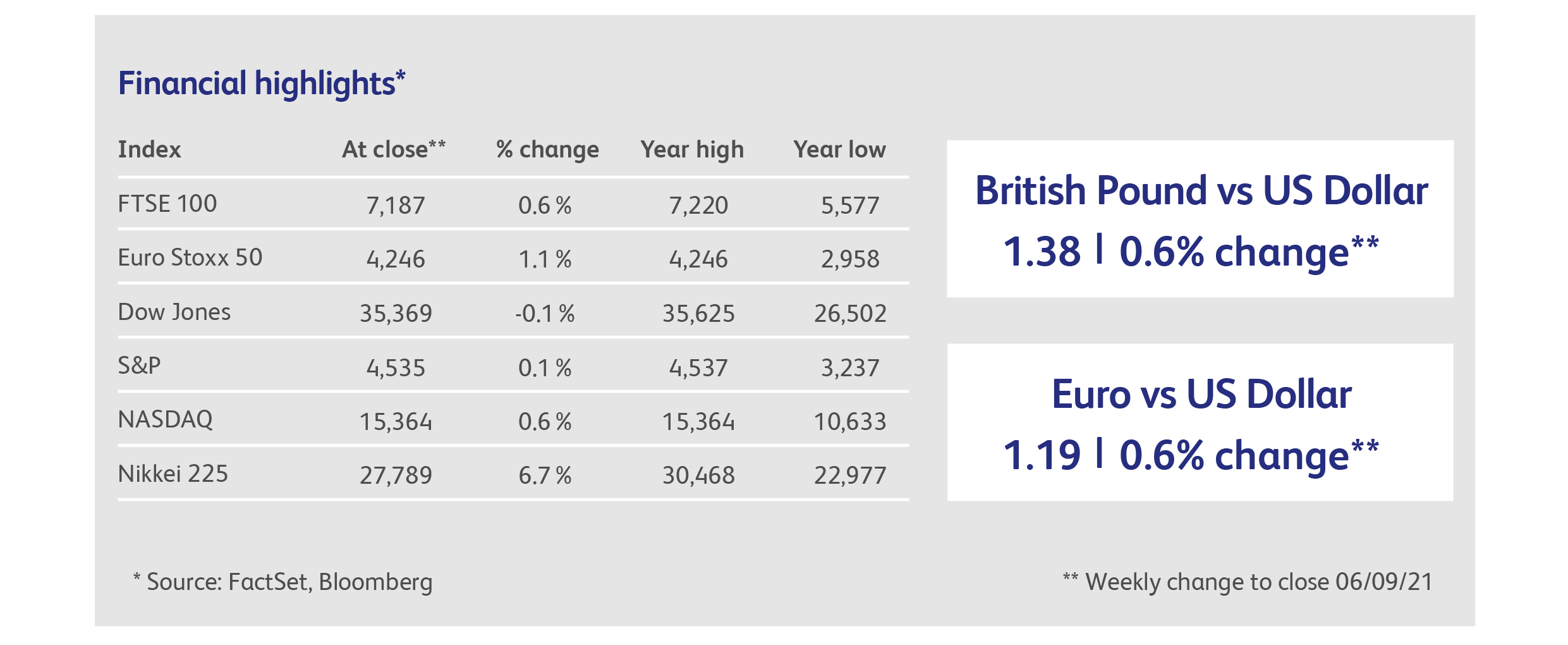

A week of unremittingly bad news failed to destabilise stock market sentiment. First up were the German and Dutch European Central Bank (ECB) governors, who upset what had appeared to be the cosiest consensus in world finance by calling for a winding-down of the ECB’s asset purchase programme. These comments echoed the ECB’s Chief Economist the previous week, who hinted that, as the asset purchase programme is “a crisis instrument", it might soon be appropriate to reduce the pace of purchases. The comments followed another upside surprise in Eurozone inflation, which jumped to a 14-year high of 3.0% in July, from 2.2% in June. European government bond yields did the obvious thing and jumped on the news, with Greek and Italian bonds faring worst. Absent the ECB, one wonders who the natural buyer is for Europe’s most heavily indebted issuers. European equities, on the other hand, were in two minds, initially gapping down a percent before recovering and then rallying to new all-time highs. All will be revealed when the ECB meets this week.

The authoritarian drumbeat from China continued all week, with each day bringing some new form of crackdown. The week started with government restrictions on financial information posted to social media that criticise domestic economic data or republish foreign media commentaries on China’s economy “without taking a stance or making a judgment”. It ended with a ban on Chinese broadcasters employing actors and celebrity guests who have “incorrect political positions”. In-between the two, various restrictions on overseas listings and private equity were announced, interspersed with data confirming the rapidly deteriorating Chinese economy (see “Economics: highlights” below). Meanwhile, Chinese technology companies were queuing up to sign up to President Xi’s vision of “common prosperity”. Tech giant Alibaba Group was the latest “willing” participant, pledging $15.5 billion over five years in donations.

Economists had already spent the week cutting their estimates for US economic growth after a slew of weak recent data, followed by plunging consumer confidence and business activity surveys, but even these dismal forecasts proved to be too optimistic when the US employment numbers for August were announced. Only 235,000 jobs were created in the US in August, far below the average expectation for a rise of 733,000, and lower than any of the estimates of the 70 economists whose forecasts are tracked by Bloomberg. US government bonds, traditionally a safe haven, continued their recent, bizarre behaviour by selling off on the news. After only a slight wobble, US equities rallied to end the day flat. Below the index level, some analysts pointed to a rotation from cyclical, economically-sensitive stocks to less-volatile sectors of the economy.

The Biden administration, meanwhile, strengthened an initiative to target anti-competitive practices by corporate behemoths, and democratic politicians proposed a range of taxes targeting corporations and the wealthy, including new taxes on stock buybacks, carbon emissions and executive compensation. Perhaps investors are right to have ignored these – after all, the debacle in Afghanistan has practically eliminated any chance of the democrats holding onto Congress and the Senate in the mid-term elections. And there was a bright spot in all the glumness: the US government proposed another $65 billion in expenditure to prepare the country against future pandemics.

Shares in Chinese online taxi-hailing service Didi Global, which have been under the cosh recently as Chinese regulators investigated its usage of customers’ data, spiked as much as 9% in its New York listing after rumours spread that the municipal government in Beijing intends to take a controlling stake.

China has banned celebrities! Or, at least, the wrong-thinking kind. The Chinese entertainment industry was thrown into a tizzy after President Xi Jinping ordered it not to employ actors and celebrity guests who have “incorrect political positions”. The Chinese listed media sector was largely boosted by the news, however, perhaps because it is involves a relatively mild impact compared with other sectors in the government’s crosshairs.

Germany’s biggest stock market index – the Dax - is getting its first makeover since its inception in the late 1980s. The index will be expanded from 30 to 40 constituents, adding about EUR350 billion in market value and including firms such as online fashion retailer Zalando, meal-kit supplier HelloFresh, Siemens Healthineers, Sartorius, Porsche, Airbus and Puma. The changes were prompted by the collapse of Wirecard a year ago, the first Dax constituent to file for bankruptcy.

The entire Japanese stock market was lifted by Prime Minister Suga’s decision to resign, with the market capitalisation-weighted Topix index reaching its highest level since the boom in 1989. The Topix and Nikkei indices are now up 8% in the last two weeks. It’s hoped that any successor will be more likely to ramp up fiscal stimulus programmes. The former Foreign Minister, who plans to run for leader, has vowed to spend tens of trillions of yen on tackling the virus.

Highlights

Only 235,000 jobs were created in the US in August, far below the average expectation for a rise of 733,000, and lower than any of the expectations of the 70 economists whose forecasts are tracked by Bloomberg. Expectations for US economic growth are being recalibrated, downwards.

Despite plenty of advance warning in recent business surveys, economists were flat-footed by a plunge in the latest Chinese business activity “Caixin” survey, one which predominantly covers the private sector.

Declining retail sales in the Eurozone threaten Europe’s status as the last bastion of accelerating economic growth, following recent retrenchments in Asia, the US and UK. Sales plummeted by 2.3% between June and July, well below expectations.

Calendar

UK GDP is expected to have grown by 0.5% between June and July, down from the 1% rate of growth experienced in the previous month. Robust increases in industrial production and construction are likely to have been offset by slower growth in services. Data already-released show that retail sales and car sales both fell sharply in July, while the decline in the number of people receiving Covid-19 vaccinations points to a decline in output in the healthcare sector.

The European Central Bank is expected to leave its main refinancing and deposit rates unchanged at its September meeting this week, but recent public announcements by ECB officials have suggested that a reduction in the pace of asset purchases is a possibility.

This publication is intended to be Walker Crips Investment Management’s own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority and is a member of the London Stock Exchange. Registered office: Old Change House, 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.