26 April 2022

A lacklustre week for stock markets was dwarfed by another wave of panic in bond markets, as the US central bank turned up the volume on its inflation-fighting rhetoric. A two-year US government bond now yields about 2.7%, and yields have only been higher than that once since before the Credit Crunch. US government bonds have now had their worst start to a year since the early 1970s. Bond markets crumpled under the onslaught from Federal Reserve officials: one governor advocated for a rate rise of 0.75% at the next meeting, and several others were heard to endorse the idea of 0.5%. This was subsequently reiterated by the Federal Reserve’s Chairman, who also upset markets by describing the American labour market as being “unsustainably hot”.

The pain has penetrated far beyond government bonds, however, and has been felt far beyond American shores. In what looked suspiciously like a coordinated global approach, a number of governing council members of the European Central Bank echoed the Fed’s enthusiasm for rate rises. Europe’s corporate bond market is going through its worst ever sell-off, with even the best-rated debt down 9% from its highs in August last year. This is a worse decline than at the start of the pandemic or during the Credit Crunch, and has wiped out five years of gains.

It’s not often the case that bonds perform worse than equities when markets sell off, and the consequences are evident in global bond issuance. The corporate bond market is still open for business as companies report strong results for the first calendar quarter, but that debt is becoming more expensive. The biggest US banks rushed to raise money following their results announcements, paying a premium to their usual yields. The fear is that they may have used up valuable demand, as investors continue to pull money out of US investment-grade bond funds. The riskier high-yield debt markets have already ground to a halt, with issuance diving to the slowest rate since 2008. Sales of high-yield debt in 2022 are expected to decline by about 60% from last year’s record levels. Bond investors are consoling themselves with the prospect of new issuance at far better yields.

Investors hoping to buy Chinese assets at cheap valuations have been disappointed, after the government’s promised stimulus failed to materialise. It’s normally a case of when the Chinese government says “jump”, investors ask “how high?”, and the Hang Seng China Enterprises Index had bounced nearly 30% from its lows in mid-March after the government promised to “actively introduce policies that benefit markets”. However, the Chinese authorities seem happy to undermine their own message to markets: interest rates have not been lowered in line with expectations, a highly-anticipated economic stimulus package has failed to materialise, and there has been no let-up of restrictions on lending in the property market. An explanation for the government’s caution may lie in its fear of inflation, after the governor of China’s central bank publicly reiterated its commitment to stable prices, and pledged support for smaller firms rather than the broader economy.

Tesla’s share price held up amidst broader market weakness, after the company announced better-than-expected results for the first calendar quarter. Like its more conventional rivals, Tesla benefited from an increase in operating margins as the global reduction in the supply of cars has enabled manufacturers to command higher prices. The company has raised prices on its cars 12 times in the last two years. Founder Elon Musk also announced that the company is working on a “robotaxi” without a steering wheel or pedals.

Elsewhere in the car industry, the European Automobile Manufacturers’ Association reported that new car registrations had fallen by 19% in March, their ninth consecutive monthly decline. Analysts attributed the unexpected slowdown to production shortages, exacerbated by the war in Ukraine, rather than to a lack of demand. Finally, a Mercedes prototype electric car drove more than 600 miles on a single charge using a new battery technology.

The travails of the streaming services continued, after Netflix announced that it had lost 200,000 customers in the first calendar quarter. The company had been expected to add 2.5 million customers during the current year, and the share price promptly fell by over a third. The company announced that it is experimenting with ways to sign up viewers who currently share someone else’s password. Netflix is now down over 60% for the year, making it the worst performer in the S&P 500 index. Disney has not fared much better following the launch of its Disney+ streaming service during the pandemic: it is down over 20% for the year and is the worst performer in the Dow Jones Industrial Index.

The European Union finalised its new regulations for social media companies, known as the Digital Services Act, which will involve massive fines for failing to address illegal content on social media platforms. Regulatory failure could cost the big tech companies up to 6% of global annual sales. The rules are expected to become law in 2024. The biggest players will also have to pay Brussels fees to cover the cost of enforcing the regulations.

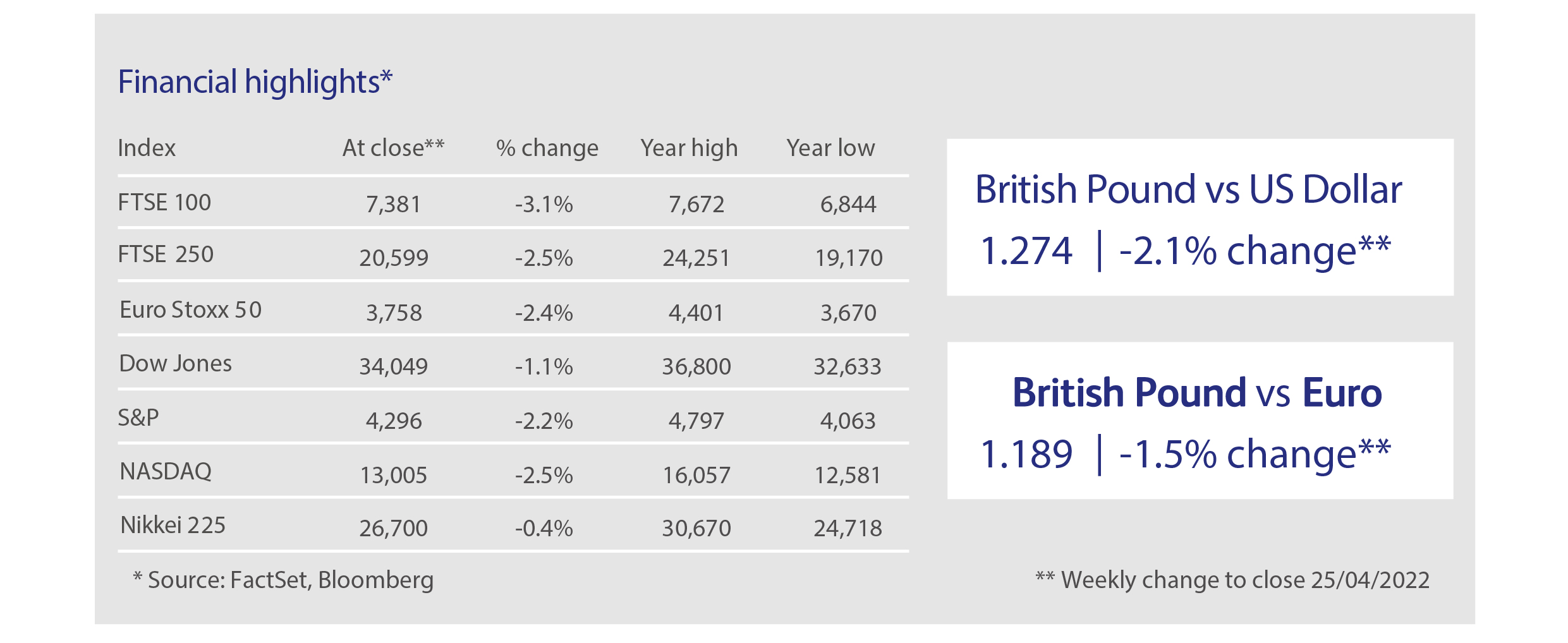

Highlights

Calendar

This publication is intended to be Walker Crips Investment Management’s own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority and is a member of the London Stock Exchange. Registered office: Old Change House, 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.