13 September 2022

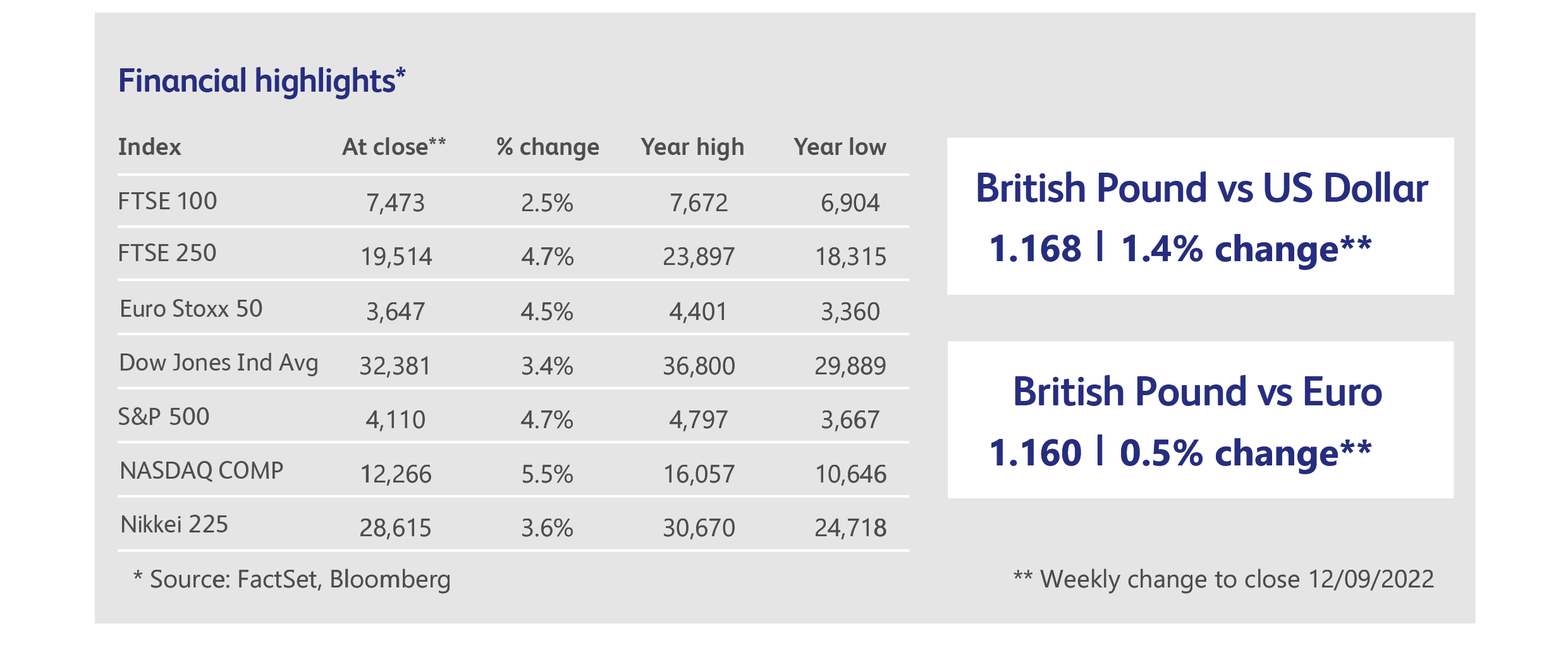

Stock markets broke their losing streak with impressive rallies across-the-board globally, despite more tough talk by central bankers and the absence of a recovery in bond markets. European stock markets recovered all their losses caused by last week’s total suspension of natural gas supplies from Russia to Europe and, counterintuitively, European gas prices have actually declined by nearly 50% since then. American petrol prices, meanwhile, fell to their lowest levels of the past six months.

The week started with more worries about economic growth, with unexpectedly weak export data from China reflecting a slump in demand elsewhere in the world, and with lacklustre Chinese imports reflecting a lack of demand within China itself. China’s economic woes have contributed to a significant recent weakening of the renminbi, forcing the People’s Bank of China to mount one of its strongest interventions in currency markets of the last few years. Markets are now only a month away from the 20th Party Congress, which will have huge implications not only for the People’s Republic of China but for the rest of the world. Optimists hope for a weakening of the government’s Covid-zero policies, which are hampering the government’s own efforts to revive economic growth.

The European Central Bank opted to raise rates by 0.75%, whereas markets had offered an even chance of a 0.5% rise. In doing this, the ECB emulated the US Federal Reserve’s singular focus on inflation, even to the extent of front-loading the pain to the economy. Inflation risks trump risks to growth. The ECB raised its inflation forecast significantly and lowered its economic growth forecast, pointing out that "recent data point to a substantial slowdown in euro area economic growth, with the economy expected to stagnate later in the year and in the first quarter of 2023". Investors can’t say they weren’t warned and, indeed, data shows that professional fund managers withdrew $3 billion from European equity allocations during the week, taking outflows over the past six months to $83 billion. Just for good measure, there was the usual round of public pronouncements by central bankers expressing their commitment to faster rate rises.

Nevertheless, stock markets rallied. Moreover, perhaps more importantly, the US dollar fell. The dollar’s safe haven status has never been more in evidence than over the past year, and its sudden, 2% weakening last week was a cause of celebration for market bulls and, indeed, anyone who pays their bills in dollars. The publication today of American inflation data for August will help confirm whether currency markets were right. While fuel prices are currently the biggest driver of inflation, the strong dollar should ultimately be the cause of its own demise as it reduces the cost of imported goods into America and, with it, inflation.

Opinions differ on whether Ukrainian advances into Russian-held territory will help or hinder markets. On one hand, their unexpected success has broken the stalemate that the war had settled into and will force Russia to change strategy. This could hasten the end of the war. On the other hand, Putin now faces a more serious threat to his leadership and could choose to bolster Russia’s involvement in order to save himself.

Analysts following Apple, the world’s largest company by market value, were underwhelmed by the launch of the iPhone 14, describing its new features as incremental rather than ground-breaking. Notably, Apple surprised analysts by not raising prices, despite the undoubted power of its brand, and even unveiled a range of promotions via its partners in the telecommunications industry.

The US Justice Department’s antitrust lawsuit against Google is expected to formally commence next year but, in a preliminary hearing, antitrust officials alleged that Google makes billions of dollars a year in illegal payments to mobile phone manufacturers to incentivise them to maintain Google as their default search engine. For its part, Google argued that its competition does not just include other search engines, but any social media platform where users can search for information.

Software maker Oracle Corporation released results that bode well for the software sector when third quarter earnings season swings into gear next month. Oracle grew its quarterly revenues by 18%. The company’s cloud infrastructure business, which allows customers to store and use information held on Oracle’s servers, saw revenues grow by 45% and now represents nearly a third of the entire business.

The price of oil fell to its lowest level in six months, despite the ongoing war in Ukraine and an output cut announced by OPEC. Commentators pointed to concern over China’s economy, the potential negative impact on demand in the developed world from interest rate rises and, finally, the strength of the dollar as the likely drivers of the decline.

Highlights

Calendar

This publication is intended to be Walker Crips Investment Management’s own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority and is a member of the London Stock Exchange. Registered office: Old Change House, 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.