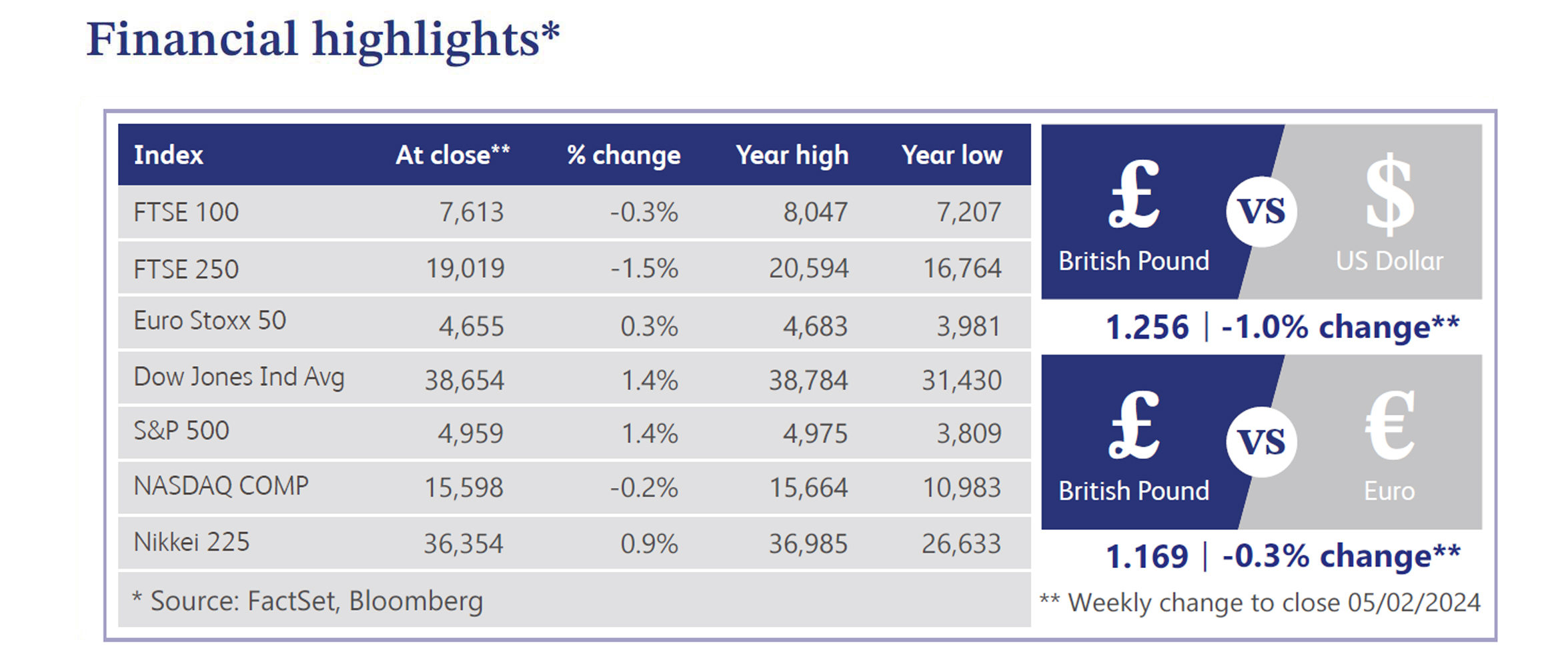

6 February 2024

Market News

Last week the Bank of England ("BOE") voted to keep interest rates steady at 5.25%. The decision represented a rare divergence of opinion with the Monetary Policy Committee split three ways for the first time since the 2008 financial crisis. Two committee members advocated for a 0.25% interest rate hike, another voted for a 0.25% interest rate cut, while the remaining six members opted for the status quo. The BOE affirmed the need for a restrictive monetary policy to address inflationary pressures, yet hinted at a forthcoming review on the duration of the current interest rate levels.

Inflation projections add to the BOE’s cautious stance. Anticipated inflation dynamics suggest a temporary fall to the 2% inflation target in the second quarter of 2024, followed by an uptick in the subsequent quarters. Geopolitical factors and wage risks are acknowledged as potential pitfalls, reinforcing the central bank's guarded approach. Nevertheless, a more positive outlook emerged for economic growth, reflected in revised gross domestic product (“GDP”) forecasts. The latest projections indicate a growth of 0.25% in 2024, a notable improvement from the earlier forecast of 0%. Furthermore, optimism extends to 2025, with GDP expectations revised upwards to 0.75%, compared to the previous estimate of 0.25%.

In addition, the BOE is scrutinising risks in the private credit market, considering factors such as revaluing assets, higher interest rates and potential impacts on financial stability. Private credit, having grown four-fold since 2015, raises concerns, especially regarding the refinancing of existing debt amid changing economic conditions.

A record number of UK firms issued profit warnings in the final quarter of 2023, surpassing levels seen during the 2008 financial crisis. Research by EY-Parthenon revealed 77 profit warnings, with a third coming from companies with annual revenue over £1 billion. Fragile demand and higher interest rates, coupled with delays in spending, contributed to this unprecedented scenario. On another front, the UK construction sector faces a challenging period, with 4,370 firms collapsing over the past year due to increasing costs of borrowing affecting profit margins. The sector anticipates continued difficulties in 2024/25.

The UK housing market has stalled, forcing vendors to slash asking prices by 10% or more, particularly in London and the South East. A fifth of sellers have resorted to significant price reductions. However, a rapid rebound in activity is not anticipated, given lingering affordability constraints. A survey conducted by the Royal Institution of Chartered Surveyors paints a mixed picture for the construction sector, with marginal improvement in late 2023, influenced by the prospect of interest rate cuts. Infrastructure activity grows, while home-building contracts further.

Pets at Home Group, the UK-based pet care business, saw its share price decline by approximately 9.9% last week after the company announced its third quarterly results. The company lowered its profit before tax guidance, now expected to be £132 million for the year, compared to the previous estimate of £136 million. This is as a result of the difficult economic environment and retail business growth falling below management expectations.

GlaxoSmithKline, the global biopharma company, reported its final quarter results last week, which saw the share price close the week approximately 4.8% higher. The company reported that it now expects revenue growth of between 5% to 7% in 2024, with earnings per share growth of between 6% to 9%. Overall, the company reported a strong set of results, maintaining a continued strong focus on margin improvements, alongside continuing to invest in further growth. Analysts largely viewed these results positively.

Diageo, the UK-based international manufacturer and distributor of premium drinks, saw its shares close the week approximately 3.1% higher as the company reported its latest set of quarterly results. The results were broadly in line with analyst expectations, with net sales at $11 billion in comparison to expectations of $10.9 billion. The company also raised its dividend by 5% to 40.5 cents per share alongside completing $500 million of share buybacks in the six months to 31 December 2023. Overall, the company reported a reasonably strong set of results in challenging market conditions.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority and is a member of the London Stock Exchange. Registered office: Old Change House, 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.