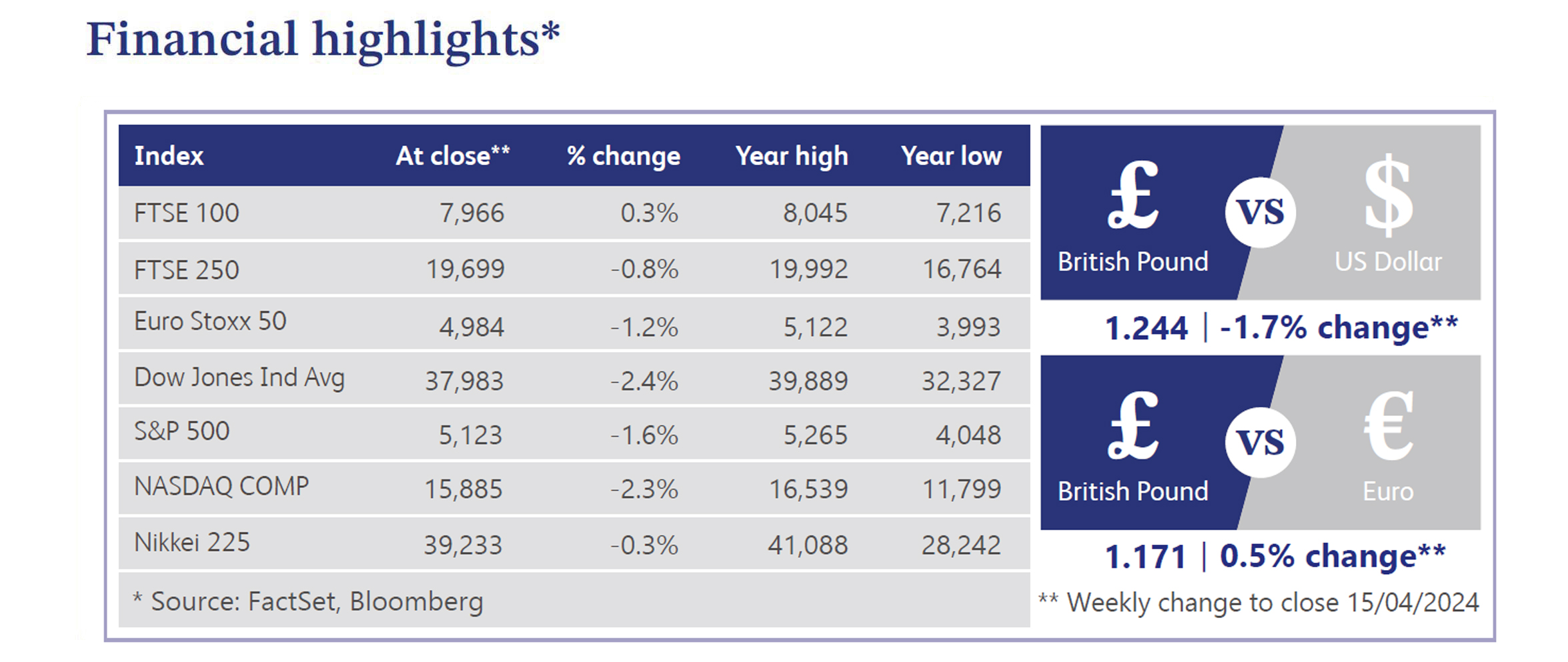

16 April 2024

The former Chair of the US Federal Reserve, Ben Bernanke, has offered a candid assessment of the Bank of England's (“BOE”) forecasting processes, highlighting shortcomings such as outdated modelling software and staff carrying out manual functions which could be automated. While providing recommendations for improvement, Bernanke stopped short of advocating major departures from the BOE's traditional approach to monetary policy, leaving such reforms for future consideration. As discussions within the central bank continue, the review marks a pivotal moment for reassessing the UK's monetary policy framework.

Meanwhile, the International Monetary Fund (“IMF”) has issued a cautionary note to the BOE, warning against maintaining high interest rates for an extended period. The IMF's forthcoming World Economic Outlook highlights the potential risks associated with a high proportion of UK homeowners on fixed-rate mortgages, emphasising the need for prudent monetary policy adjustments to mitigate adverse economic impacts. With over 80% of homes in the UK on fixed-rate mortgages, and approximately 1.5 million expiring in 2024, the IMF underscores the importance of timely policy responses to evolving market dynamics.

In parallel, traders have toned-down expectations on the number of rate cuts this year, with only two cuts now predicted in 2024. Recent data releases, including US Consumer Price Index data and hawkish comments from BOE Monetary Policy Committee ("MPC") member Megan Greene, have contributed to this shift in sentiment. While a rate cut was previously anticipated as early as May or June, the current outlook suggests a potential delay, with investors aligning their expectations more closely with the US interest rate market. Furthermore, renewed concerns over the London equity market have emerged following warnings from Shell's CEO regarding the possibility of a primary listing relocation, raising apprehensions about the potential exodus of energy and mining firms from the FTSE 100.

Despite these uncertainties, some investors see value in betting on the BOE to cut rates ahead of the European Central Bank and the Federal Reserve. A Bloomberg article reported that Jupiter Asset Management, Pictet and Candriam are among those who believe that the market is underpricing the likelihood of the BOE delivering faster and deeper rate cuts compared to other major central banks. However, BOE MPC member Greene has cautioned against premature rate cuts, emphasising the need to monitor ongoing inflationary pressures and supply constraints within the UK.

Fresnillo, the precious metals mining company, saw its share price surge approximately 14.9% last week. The positive performance appeared to be largely driven by the recent silver and gold price rally. During April, gold has seen its price surge by approximately 5.2% and silver has witnessed an increase of approximately 13.1%. This has led to positive sentiment regarding higher pricing for Fresnillo’s key products, which is expected to drive higher earnings.

Rio Tinto, the world’s second-largest metals and mining company, saw its share price end the week approximately 8.1% higher. The company announced last week that it has secured funding of $15 billion for the Simandou iron ore project in West Africa. The company noted that the project is the largest untapped reserve of high-grade iron ore, with guidance of over two billion tonnes.

Centrica, the British multinational energy and services company, saw its share price increase by approximately 7.5% last week. The company announced last week that it had signed a 10-year power purchase agreement with STMicroelectronics, a global semiconductor leader, for the supply of renewable energy to its operations in Italy, starting in January 2025. The agreement includes the sale of approximately 61 GWh of renewable energy per year by Centrica, which is produced by a new solar farm in Italy.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management’s own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: Old Change House, 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.