24 February 2026

Last week, Bank of England (“BoE”) Monetary Policy Committee (“MPC”) member Catherine Mann signalled she is edging closer to backing an interest rate cut, with markets now fully pricing in two reductions by year-end as inflation eases to 3%. The UK labour market is cooling, with unemployment at a cycle high of 5.2%. Small businesses anticipate job cuts due to April's increases in minimum wage and National Insurance. Political uncertainty persists amidst speculation that Manchester mayor Andy Burnham may challenge Prime Minister (“PM”) Keir Starmer. Despite this, institutional investors such as Schroders are increasing UK debt exposure, buying longer-dated gilts, believing monetary policy will outweigh near-term political risks.

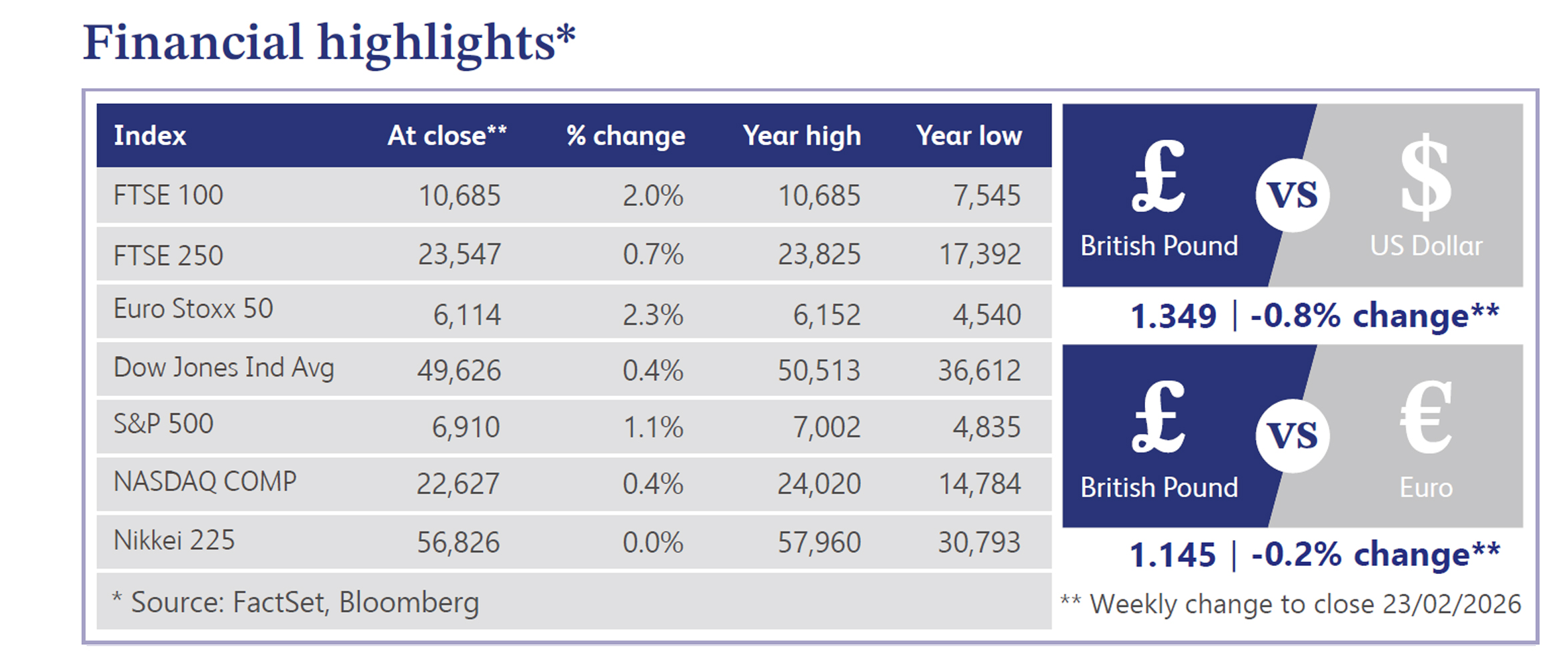

In equities, the FTSE 100 index finished the week up to 10,684.74, bringing its year-to-date gain to 7.12%. Meanwhile, Chancellor Rachel Reeves received a boost ahead of her Spring statement as UK public finances recorded a record £30.4 billion January surplus, beating the Office for Budget Responsibility (“OBR”) forecast. This was driven by higher income and capital gains tax receipts and lower debt-interest costs. Despite this fiscal headroom, Reeves is expected to announce no new tax cuts to restore market confidence. Reeves is resisting PM Starmer and the Ministry of Defence's calls for accelerated military spending to cover a £28 billion shortfall. Globally, the UK is lobbying European Union allies against French-pushed "Made in Europe" proposals, warning they could block UK public procurement in tech and renewables, risking harm to competitiveness and investment. In currency markets, sterling weakened against the dollar to 1.3491.

Across the Atlantic, economic data generally reflected a firm backdrop, with the first read of fourth-quarter US gross domestic product (“GDP”) coming in softer than expected (1.4% vs 2.7% expected), while December core Personal Consumption Expenditures (“PCE”) printed as anticipated (+0.4%), albeit higher than November. Initial jobless claims were softer than forecast, and January's industrial production was a bright spot, arriving well ahead of December's downwardly revised level. Consequently, major United States equity indices moved higher during the holiday-shortened week; the Dow Jones Industrial Average rose 0.4%, the S&P 500 gained 1.1%, the Nasdaq increased 0.4%, and the Russell 2000 added 0.65%. Big tech was mostly positive, highlighted by Amazon climbing 5.7%. Macro sentiment centred on central bank policy, with Federal Reserve (“Fed”) funds futures still fully pricing in two 25 basis point rate cuts this year. Treasuries were narrowly mixed with the curve flattening, the DXY rose 0.9%, and gold finished up 0.7%. WTI crude oil settled up 5.7% after two weekly declines, driven by potential US military action in Iran; President Trump urged Iran to agree to a nuclear deal within 10-15 days to avoid an "unfortunate" alternative.

UK house prices stalled in February after a 2.8% January rise, as early demand faded and the market responded to fundamentals. Buyers have stronger bargaining power, with homes for sale at an 11-year-high. Agreed sales are up 9% from 2024, and asking prices are 2.8% above December. Developers believe UK residential land values are nearing a floor, with late-2025 seen as the low point, supported by easing borrowing costs and planning reforms.

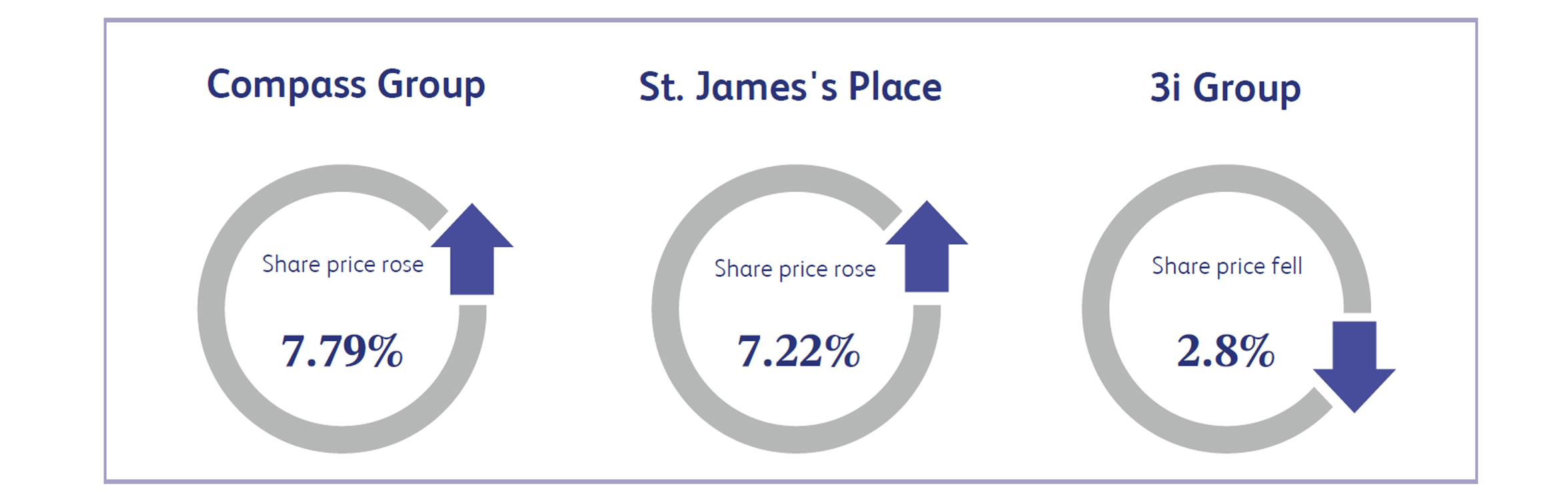

Compass Group, the multinational contract catering and food service company, surged 7.79% after releasing a strong trading update that revealed first-quarter organic revenue growth jumped 7.3%, beating market expectations. The performance, which highlights the firm's robust 96.3% client retention rate and the successful, ahead-of-schedule integration of recent acquisitions, underscores the underlying strength and reliable earnings power still present within UK blue-chip firms despite the broader sluggishness of the London market. This upward momentum further validates the appeal of high-quality market leaders, as investors capitalise on attractive growth prospects to back proven, globally diversified operators, effectively rewarding one of the exchange's most consistent performers.

St. James's Place, the British wealth management business, rose 7.22% after a major brokerage upgraded the stock to a "buy," citing its highly attractive valuation following a recent tech-driven sell-off. The upgrade, which highlighted the firm's robust medium-term earnings growth potential and the successful implementation of its new charging structure, underscores the underlying resilience and reliable cash generation still present within UK financial stalwarts despite broader market anxieties over artificial intelligence disruption. This positive assessment from a major financial institution signals confidence in the company's strategic direction and its ability to maintain a competitive edge in an evolving technological landscape.

3i Group, the British private equity and infrastructure investment company, fell 2.8% after analysts downgraded the stock over valuation concerns regarding its key portfolio holdings. The downgrade, which highlighted fears that its largest retail investment is moving into a period of diminishing returns due to macroeconomic pressures on consumers, underscores the underlying vulnerability still present within United Kingdom investment trusts despite the broader resilience of the London market.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.