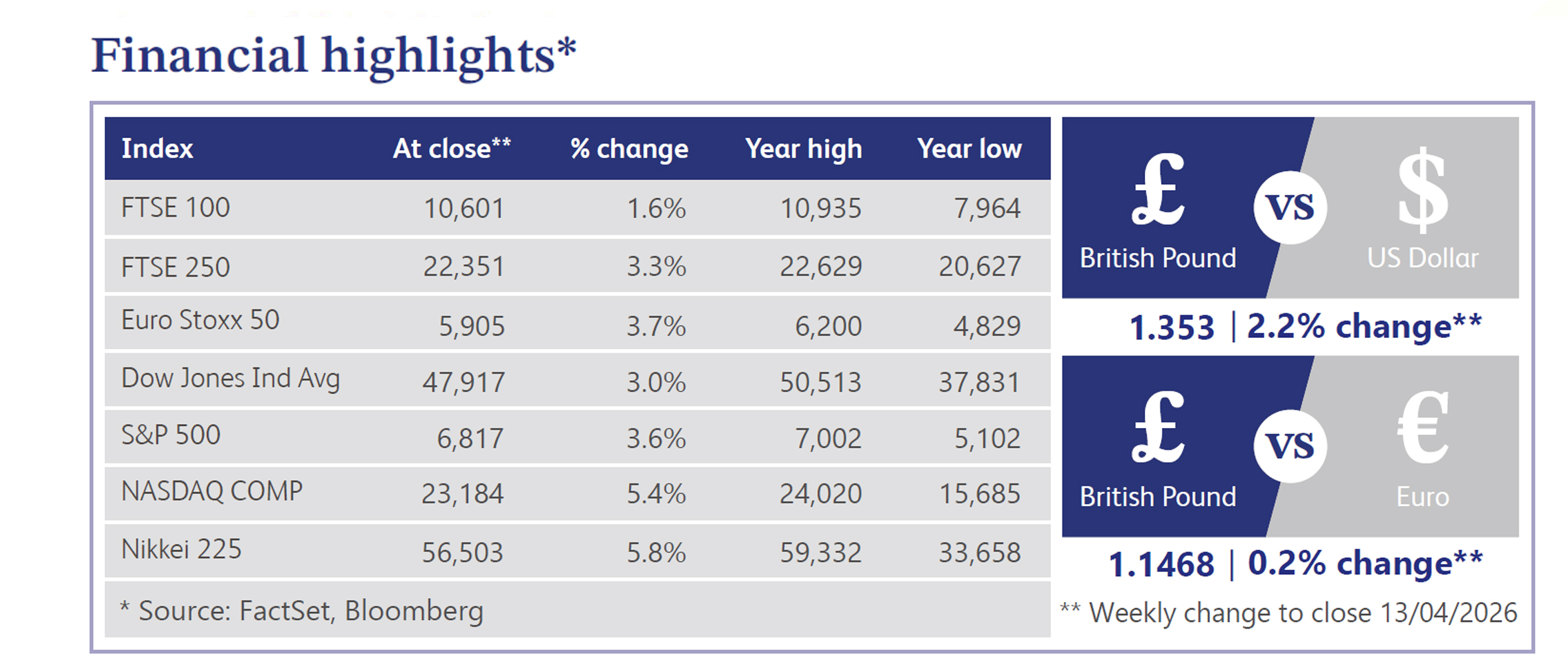

14 April 2026

In the wake of the Middle East conflict, the UK economy is signalling heightened stagflation risks. This was backed by warnings from shipping experts, who noted that supply chain fractures guarantee at least six months of elevated food and fuel prices. The final composite Purchasing Managers' Index ("PMI") set to a six-month low of 50.3 as 40% of firms reported rising costs. Even with a fragile US-Iran ceasefire holding at the time of writing, the Bank of England ("BoE") faces a severe policy dilemma.

Starmer is trying to get a grip on the geopolitical crisis by using the instability as political cover to prioritise homegrown energy investment, especially as Downing Street remains deeply frustrated by unpredictable US policy and direct threats to British energy costs. Fiscally, Chancellor Rachel Reeves is navigating a challenging fiscal environment stubbornly resisting union demands for public sector pay rises and holding the line at a 2.5% settlement to avoid adding £5 billion to the wage bill. This strict discipline is maintained even as the Organisation for Economic Co-operation and Development ("OECD") warns that the convoluted tax trap remains a major drag on domestic employment.

Whilst financial markets are pricing in this geopolitical fragility, it left the City in a deep freeze. Retail investors pulled £1.4 billion from equity funds in March, and the London initial public offering ("IPO") market caved with just two minor listings. In the markets, sovereign debt remains the epicentre of volatility, as Gilt markets suffered extreme whiplash when the 10-year yield violently jumped 15 basis points. Consequently, Sterling now carries a higher geopolitical risk premium than the Euro. However, BoE Governor Bailey issued stark warnings that a sudden loss of confidence could fracture the leveraged private credit sector. The geopolitical macro is translating directly to sector divergence; manufacturing faces a £939 million business rates hike threatening 25,000 jobs, whilst construction remains stalled by high material costs.

Across the pond, major US indices climbed for consecutive weeks and neared all-time highs as the US-Iran ceasefire held. Big tech and semiconductors outperformed on surging AI demand, spurred by significant partnership announcements, whilst software lagged due to renewed disruption fears. The Iran conflict remained the primary driver of market sentiment; despite plunging oil prices easing inflation concerns, shipping through the Strait of Hormuz remained stalled ahead of complex peace negotiations. Treasuries saw mixed results following a lacklustre auction, the dollar weakened, and gold advanced. Even though WTI crude suffered its largest weekly drop in recent years, broader retail investor participation was heavily tempered as dip-buyers sold into the rally, operating alongside hawkish Federal Reserve minutes and record-low consumer sentiment.

Macro pressures from the Iran conflict and volatile BoE rate expectations have stifled housing momentum. Halifax reported an unexpected 0.5% monthly price decline in March, whilst Royal Institution of Chartered Surveyors ("RICS") data showed buyer enquiries plunging to their lowest levels since 2023. Though widespread fixed-rate mortgages continue to offer underlying resilience, analysts warn rising borrowing costs heavily weigh on near-term sentiment and caution dominates the outlook.

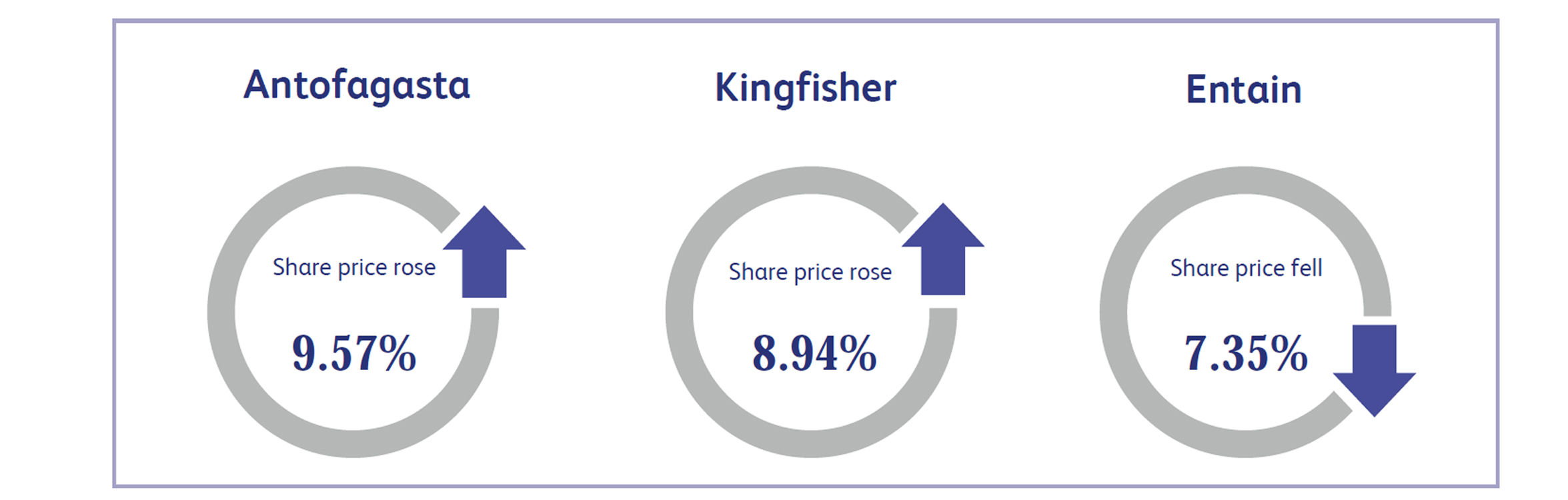

Antofagasta, a leading copper mining group, surged 9.57% this week, propelled by a sharp rally in base metal prices following a two-week ceasefire agreement between the US and Iran. This diplomatic breakthrough provided a crucial off-ramp for the conflict, easing immediate pressure on global markets and boosting copper prices. The ceasefire triggered a broader stabilisation in risk sentiment by partially restoring global oil supplies and pricing out extreme risk premiums. Consequently, mining companies dominated the FTSE leaderboard, with Antofagasta leading the charge as investors welcomed the reduced geopolitical uncertainty.

Kingfisher, a retail group that engages in provision of home improvement products and services, had its shares climb 8.94% this week after the company instructed BNP Paribas to execute the initial £75 million tranche of its £300 million share repurchase programme. The repurchases, aimed at reducing share capital, will conclude by 30 June 2026. While recent results highlighted robust sales growth, analysts cautioned that softer consumer confidence could impact future trading, prompting a slight cut to near-term profit forecasts. However, Kingfisher’s strong 4.1% dividend yield and the immediate commencement of this significant buyback scheme provided firm support for the share price.

Entain is a global sports betting and gaming group that jointly owns the North American operator BetMGM. The stock fell 7.35% this week amid a confluence of international regulatory headwinds and concerns over slowing first-quarter growth. In Australia, the government announced a severe crackdown on gambling advertisements starting in 2027, banning celebrity endorsements and strictly limiting online exposure, which directly impacts Entain’s Ladbrokes. Furthermore, analysts anticipate a sluggish first quarter update, forecasting that unfavourable US sports results and higher UK gaming taxes could see the firm undershoot its full-year guidance. Despite this, brokers note the upcoming World Cup could drive a much-needed second quarter recovery.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.