28 April 2026

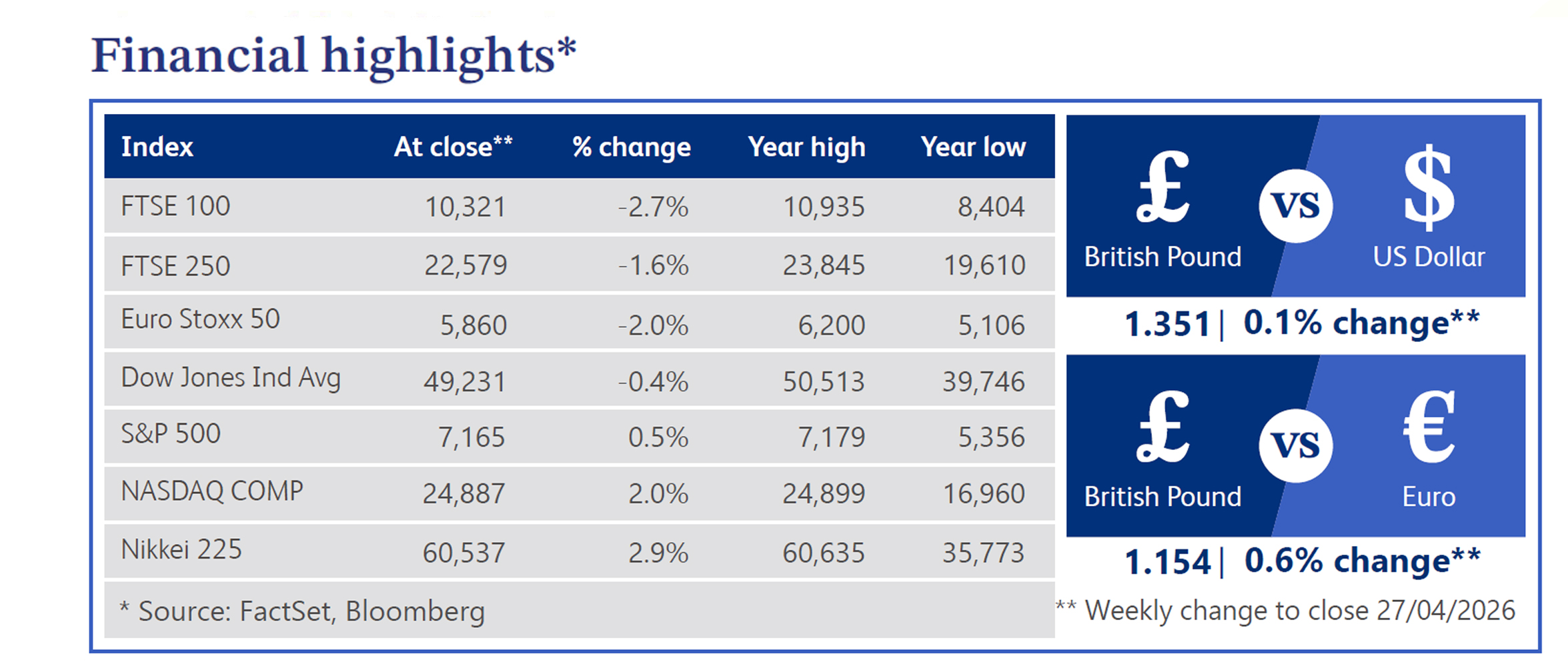

Last week, the published economic data presented a misleading picture of domestic growth. The composite Purchasing Managers' Index ("PMI") unexpectedly jumped to a two-month high, driven by corporate panic as firms are stockpiling inventory due to supply chain fears, triggering the largest monthly surge in the Input Prices Index in nearly three decades. These costs are now trickling down to consumers, with consumer confidence plunging to a record low, as headline inflation accelerated to 3.3%, aided by a spike in motor fuels and food prices. The only silver lining for the Bank of England ("BoE") is a cooling labour market with average weekly earnings falling to 3.8% and April pay settlements softening, allowing the central bank to potentially avoid a domestic wage-price spiral.

In Westminster, a think tank has warned the government that their fiscal “buffer” may shrink due to the ongoing geopolitical conflict, leaving the Chancellor Rachel Reeves with £6 billion of fiscal headroom. Stripped of the ability to deploy capital, the Treasury will resort to doubling down on fiscal discipline and regulatory reform. The government announced reforms to delink power and gas prices by hiking the windfall tax on legacy low-carbon electricity generators to 55% to subsidise household energy bills. As the government is pivoting toward closer EU alignment, it faces a transatlantic threat as President Donald Trump has once again lashed out at the UK threatening tariffs if the taxes on digital services from US Tech giants are upheld.

In the UK markets, geopolitical and domestic uncertainty are still driving sentiment. Nearly half of all profit warnings issued by listed companies in Q1 directly cited geopolitical or regulatory uncertainty. This environment has triggered broad capital flight, with domestic Fintech investment plunging to a five-year low amid tighter financings. Meanwhile, Sainsbury’s warned escalating energy costs will increase grocery prices without government action. Separately, Barclays noted relaxing bank capital rules could stimulate £15 billion in gilt demand, lowering Treasury costs.

Across the pond, US indices reached record highs for consecutive weeks as robust corporate earnings and the AI boom fuelled a historic semiconductor winning streak. However, the rally was concentrated, leaving smaller companies and defensive sectors lagging. On the monetary policy front, broader market confidence was supported by the clearing of political hurdles for the next Fed chair nominee following the conclusion of a departmental investigation. Geopolitics has again dominated sentiment as President Trump abruptly cancelled diplomatic talks, maintaining a naval blockade despite Iran’s new proposal to reopen the Strait of Hormuz. This standoff caused oil prices to surge, reversing recent declines, while gold and Treasuries faced pressure. UK house price growth forecasts have been halved as the Iran conflict and rising mortgage costs dampen sentiment. Knight Frank reported a 12% drop in property offers, while affluent investors are reportedly exiting for higher-yielding asset classes. Despite a steady rise in Rightmove’s asking prices, buyer demand has fallen 7% annually.

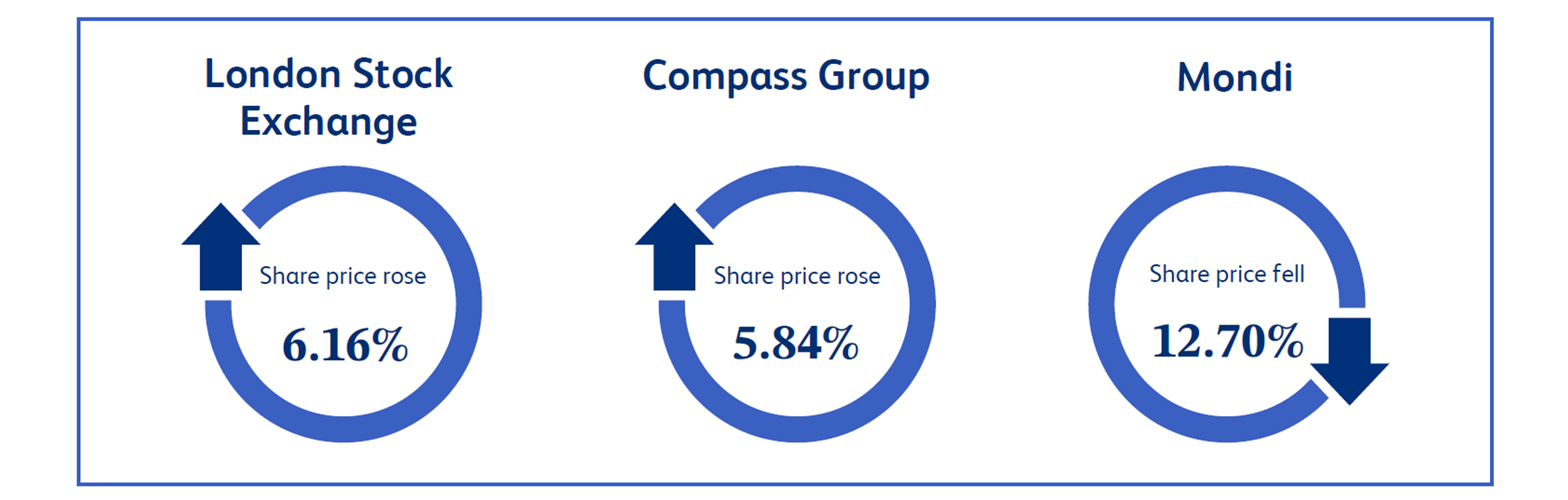

London Stock Exchange Group, which operates global financial markets infrastructure, was one of FTSE's top performers last week, surging 6.16%. The rally was driven by a strong wave of market relief as the market was wary how AI might disrupt the firm's lucrative data and analytics businesses, but management firmly put those fears to rest. The company comfortably beat first-quarter expectations and upgraded its full-year outlook, whilst demonstrating impressive traction with its own AI roll-out by rapidly onboarding customers to new platforms. The market reacted positively to this with investors viewing this as proof that the business is resilient, successfully turning a perceived threat into a long-term growth advantage.

Compass Group, a multinational contract catering and food services provider, saw a 5.84% increase in its share price on the back of favourable long-term industry projections. Rather than being driven by company-specific earnings, the stock caught a strong tailwind from newly published market research painting a robust picture for the global catering sector. The research projects steady, structural expansion over the next decade, driven by evolving supply chain practices and technological upgrades. For investors, this broader macroeconomic outlook served as a strong sentiment booster for the sector's biggest players. Seemingly the market believes Compass Group could be well-positioned to capitalise on this expanding landscape, capturing further market share and investment as the industry grows.

Mondi, an international packaging and paper group, was one of the bottom performers last week, with its shares declining 12.70%, as the company was hit by a perfect storm of rising global costs and poor timing. The sell-off came after management revealed a sharp drop in early-year profits. Tensions in the Middle East drove this decline directly. This geopolitical shock heavily increased Mondi's bills for energy, shipping, and raw materials. The company is attempting to raise its own prices to fight back. A painful operational delay means this financial relief will not arrive until later this year, and the market sentiment soured as a result. Falling timber prices in South Africa also wiped out an expected financial boost from its forestry assets, further dampening the market sentiment.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.