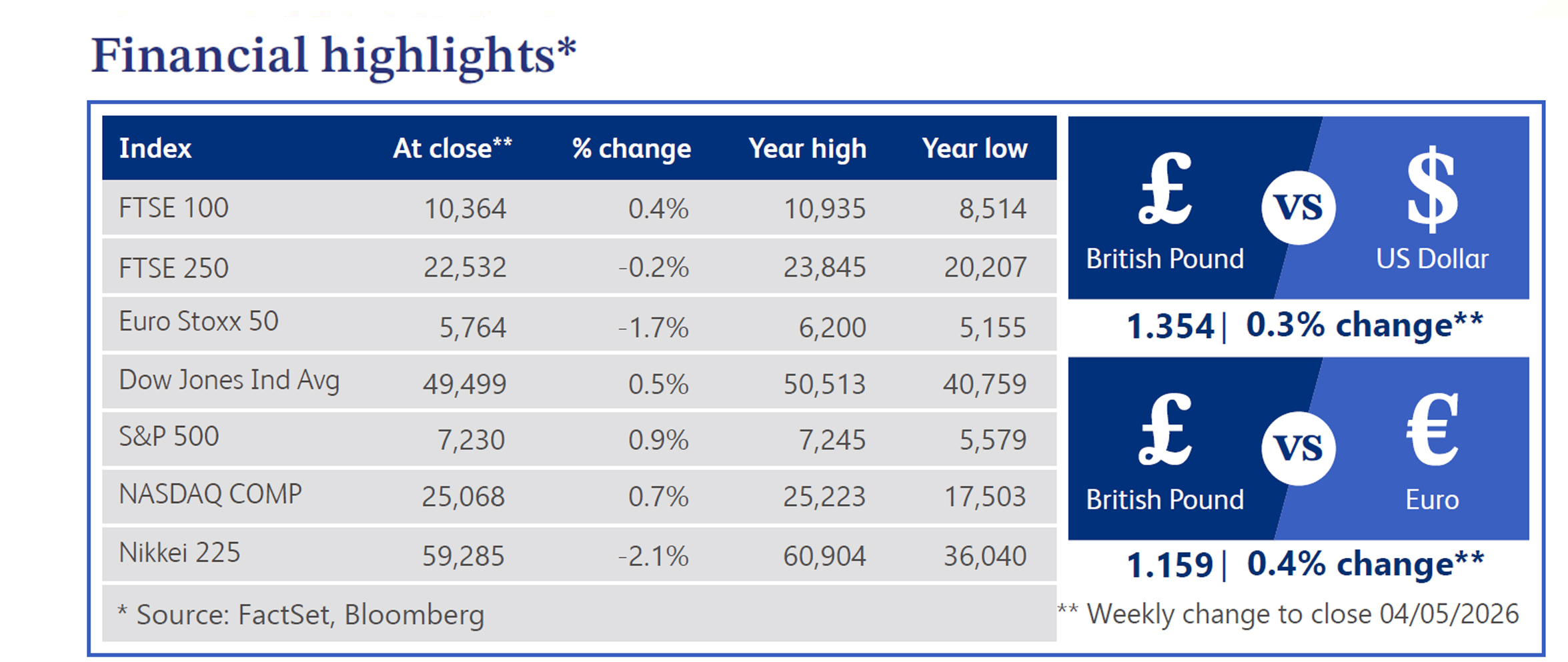

5 May 2026

Last week, Bank of England (“BoE”) Governor Andrew Bailey reiterated that the central bank is in no rush to raise interest rates. The recent surge in energy prices has created a significant supply-side shock, which Bailey and members of the Monetary Policy Committee (“MPC”) believe is better addressed through monitoring inflation risks rather than implementing an immediate tightening response. Policymakers ultimately voted 8–1 to maintain the Bank Rate at 3.75%, despite growing divisions within the committee as some members pushed for further hikes following the rise in inflation surveys.

UK government bonds came under pressure as markets reopened following Monday’s bank holiday. Benchmark 10-year gilt yields rose to 5.04%, as investors increased expectations for additional monetary tightening in response to the rally in crude oil prices amid escalating Middle East tensions. Markets are now fully pricing in three additional BoE rate hikes by year-end, reversing some easing expectations seen last week. Despite the more hawkish rate outlook, the FTSE 100 finished the week relatively flat, supported by the resilience across energy and commodity-linked sectors.

Chancellor Rachel Reeves announced a renewed growth agenda ahead of Thursday’s local elections, focusing on fiscal discipline and regulatory reform to improve competitiveness. The announcement comes amid heightened scrutiny over public finances, with the Lords Economic Affairs Committee (“LEAC”) urging the government to rebuild fiscal buffers as rising defence expenditure places pressure on the sustainability of the state pension triple lock. Political risks remain firmly in focus ahead of Thursday’s local elections and Friday’s results. Polling data cited by Sky News suggests the governing Labour Party could lose as many as 2,000 of the approximately 5,000 council seats it is contesting. Such an outcome would likely intensify concerns surrounding political instability and increase expectations for a more expansionary fiscal stance.

Across the Atlantic, macroeconomic data remained supportive of risk sentiment. Initial jobless claims fell to their lowest level since 1969, while first quarter GDP increased at an annual rate of 2.0%. Major US equity indices posted solid gains, with the the S&P 500 advancing 0.91% to a record high and the Nasdaq Composite climbing 1.12%, marking its fifth consecutive weekly gain. Technology stocks led the rally, driven by the “Magnificent Seven” companies and continued enthusiasm surrounding artificial intelligence. US Treasury prices declined as investors increasingly priced in no Federal Reserve rate cuts this year. Meanwhile, the US Dollar Index (“DXY”) weakened modestly, while gold prices retreated.

Geopolitical developments remained central to market sentiment. Despite President Donald Trump stating dissatisfaction with the latest Iranian proposal, the ceasefire continued to hold. Markets remained sceptical of any near-term escalation, even as the Strait of Hormuz remained effectively closed, with reopening timelines reportedly slipping into late summer. The continued disruption supported energy markets, sending West Texas Intermediate (“WTI”) crude oil up approximately 7.0% following tightening inventory data.

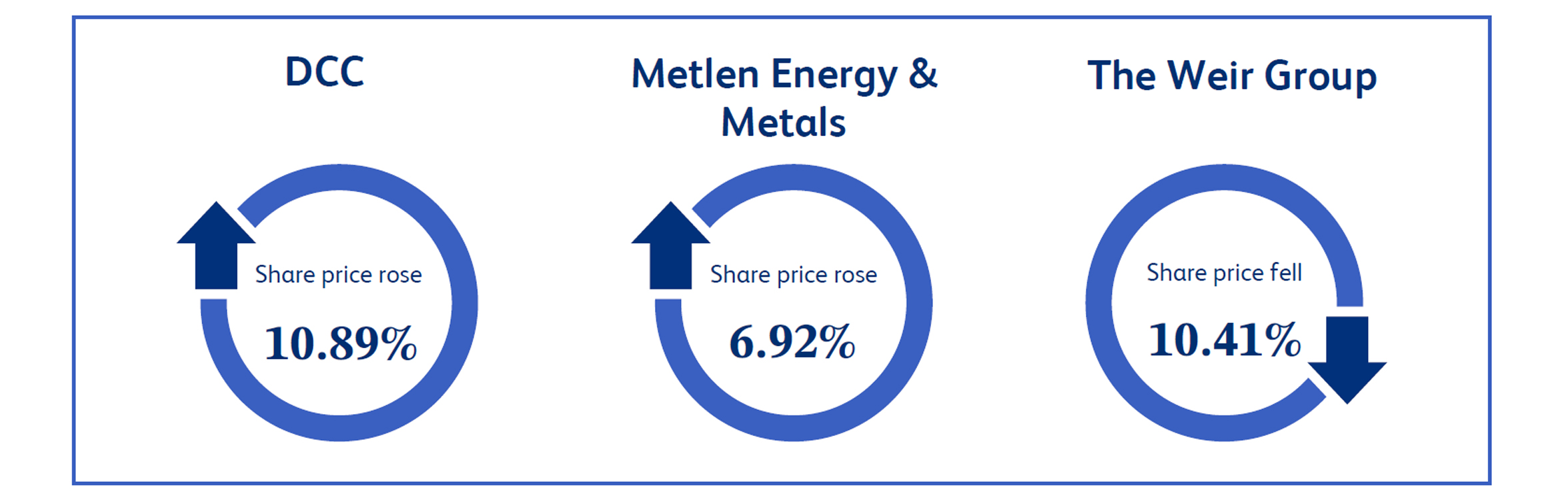

DCC, which focuses on the sales, marketing, and distribution of energy across international markets, was one of the top performers in the FTSE 100, with its share price rising 10.89% after the company received and rejected a £5 billion private equity takeover bid. The market reacted positively to the approach from US investors, viewing it as further evidence that London-listed equities remain undervalued. DCC has recently divested its healthcare and technology divisions to focus on its core energy operations. With energy prices remaining elevated, investors believe the simplified structure increases its attractiveness.

Metlen Energy & Metals, which develops and operates energy infrastructure and green transition projects, rose 6.92% following EU approval of an international energy storage partnership announced in March, alongside insider share purchases. Sentiment improved after the EU approved Metlen’s partnership with PPC Group to build a portfolio of battery storage systems across Italy, Romania, and Bulgaria. The approval strengthened confidence in the company’s expansion into the renewable storage sector, which continues to benefit from structural demand growth. In addition, an entity closely associated with the executive chairman made an open-market share purchase. This insider buying, combined with a visible pipeline of European energy projects, provided further strategic reassurance to investors.

The Weir Group, a mining technology and engineering business, was among the worst performers in the FTSE 100, with its shares falling 10.41% as investors reacted to geopolitical risks and a leadership transition. Although the company reiterated its financial guidance, sentiment was driven by concerns over operational risks linked to Middle East tensions. Management warned that the geopolitical backdrop could create uncertainty for the mining sector, including temporary operational disruptions and delayed equipment orders. This added to investor caution as macro risks increasingly fed into order visibility. Sentiment was further weighed down by the announcement that Chief Executive Jon Stanton will step down this summer after ten years in the role. The combination of geopolitical uncertainty and leadership change drove the sharp sell-off.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.