14 July 2026

Last week, Bank of England Chief Economist, Huw Pill, downplayed any near-term rate cuts, noting the central bank must keep inflation under control. Consequently, policymakers are maintaining a cautious stance, especially as Monetary Policy Committee official Megan Greene signalled a readiness to hike rates if domestic overheating persists. Elsewhere, the International Monetary Fund upgraded the UK’s 2026 growth forecast to 1%, positioning it as the third fastest-growing economy in the G7. However, this contrasted with comments from ratings agency, Fitch, that high debt and inflation-linked servicing costs constrain creditworthiness, while elevated yields reflect monetary expectations and a weaker growth outlook.

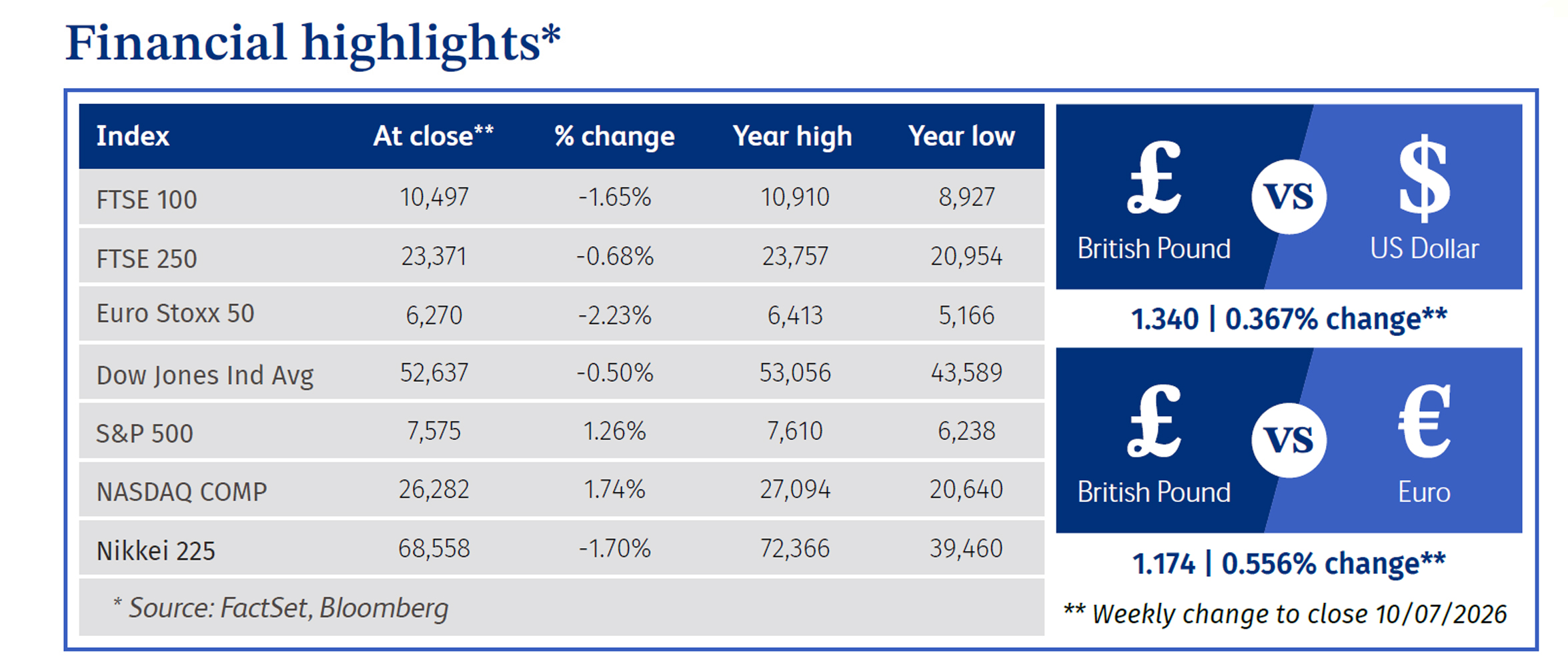

In equities, the FTSE 100 index fell last week, as the Iran war ceasefire broke down. The flare-up in the Middle East injected severe volatility into the markets, triggering sharp drops in both UK equities and gilts. Meanwhile, domestic business confidence hit a multi-month low as political uncertainty and persistent inflation fears helped keep activity suppressed. In politics, Andy Burnham is locked in to become the next UK Prime Minister after being backed by 349 Labour MPs. This sets up his “coronation” as the new prime minister on Monday, 20th July. This will make him the UK’s sixth PM in ten years and the fifth to enter office without a general election. To maintain stability, Burnham has set out further plans and rejected splitting the Treasury, choosing instead to grant Downing Street greater direct oversight of economic policy.

Across the Atlantic, geopolitics moved back into consideration, seeing several rounds of US-Iran strikes and counterstrikes. This heightened tension pushed crude to its first weekly gain since early June. The rally was further fuelled by President Donald Trump’s mid-week declaration that the US-Iran ceasefire is officially "over". Meanwhile, announcements from the Federal Reserve were muted, with officials highlighting ongoing risks from above-target inflation but overall adopting a wait-and-see attitude. In markets, major US indices were mixed, with the S&P 500 and Nasdaq both rising for the fourth time in the past five weeks. However, the Dow Jones Industrial Average fell slightly as the rising oil prices cooled the broadening-out trade that had been seen in recent weeks. Big Tech traded mostly higher, with Meta leading the Magnificent 7 after surging approximately 15% last week. The massive rally was primarily triggered by details of its upcoming artificial intelligence cloud business pivot, which successfully reframed investor anxiety over its capital expenditure cash burn into a viable revenue engine. Outside of tech, Walmart announced it would lower prices on thousands of items amid consumer affordability pressures. Elsewhere, the dollar was higher against the yen and euro, while gold dropped slightly.

Finally, UK housing showed tentative stabilisation rather than a clean recovery. The Lloyds index edged up 0.2% in June, its first rise in four months, though annual growth stayed modest at 0.6%.

Vodafone Group, a leading British multinational telecommunications company providing mobile, broadband and digital services, led the index last week as its shares rose 11.60%. This positive movement in the share price was driven by significant corporate and strategic developments, notably the announcement of a massive 16.2% stake acquisition by French telecom billionaire Xavier Niel at a substantial premium. Investor enthusiasm was further bolstered by Vodafone's expanded footprint in high-growth African mobile markets through its Vodacom unit, as well as market confidence in Neil's proven track record of driving cost-cutting and operational efficiency.

Shell, a major global energy company that produces and markets oil and natural gas, as well as renewable energy, was another strong performer, with its shares rising 5.08% last week. This increase was driven by a sharp rise in global oil prices following geopolitical disruptions near the Strait of Hormuz, alongside an expected multi-billion-dollar positive swing in the company's working capital. Investor enthusiasm was further bolstered by significant corporate and macroeconomic developments, notably the release of an upbeat quarterly trading update projecting gas trading and optimisation profits to be significantly higher than the previous quarter.

St James's Place (“SJP”), the largest UK wealth manager, was the notable laggard of the index as its shares fell 11.30% last week. The immediate trigger for the sell-off was a report stating that Sovereign Wealth, one of SJP’s largest partner firms, had decided to exit the group. Sovereign Wealth is reportedly in talks to join the Swedish wealth management group Söderberg & Partners. Market analysts flagged this exit as highly concerning as it provides the tangible evidence that SJP is facing severe adviser retention challenges following the overhaul of its charging structure in summer 2025.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.