25 May 2021

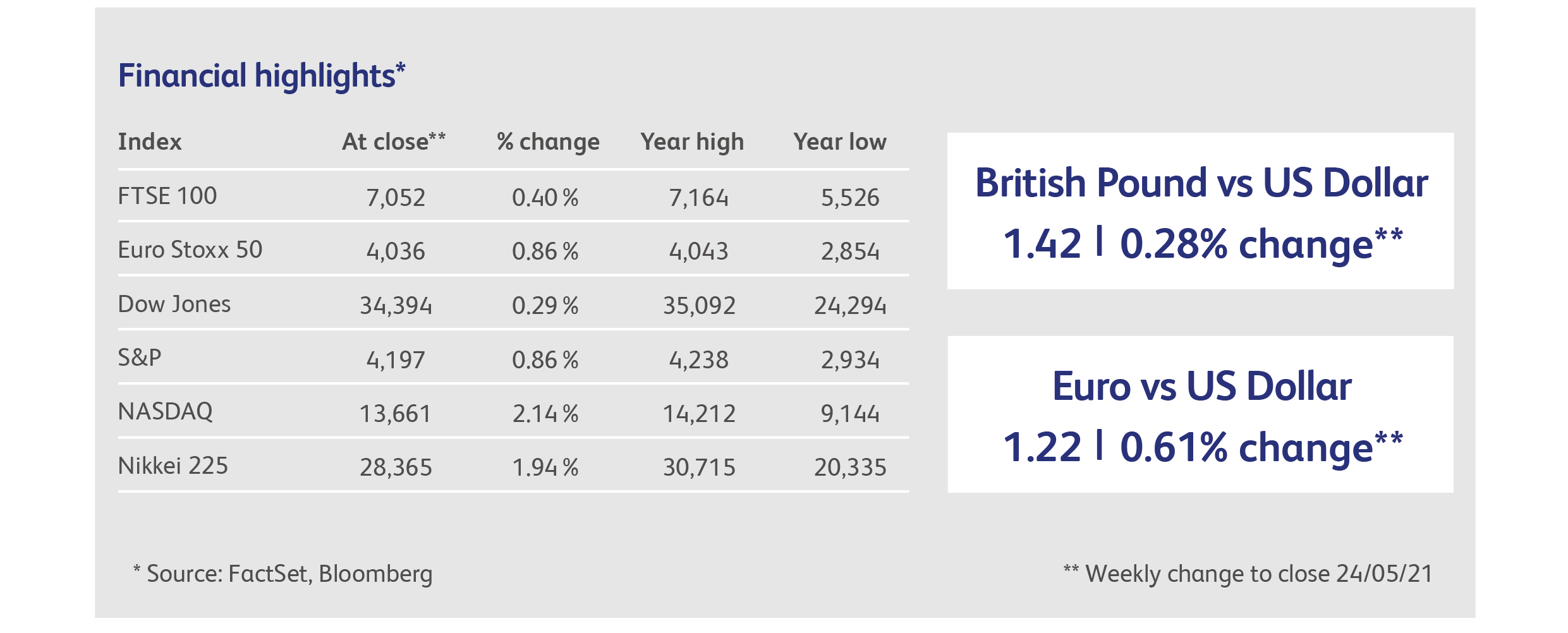

Stockmarkets resumed their upward trend last week and government bond yields stabilised, despite more signs that inflation is on the rise. One doesn’t have to look far to see inflationary threats. This week it was visible in the monthly business activity surveys for the UK and Eurozone: the UK survey’s index of output prices jumped to the highest level in its 23-year history. Also in the UK, a surge in wholesale prices for electricity and natural gas prompted economic forecasters to increase their inflation expectations. In the Eurozone, inventories in manufacturing fell at their fastest pace since 2009, as firms were forced to run down existing stock to satisfy customers. In Germany, 80% of manufacturing firms now report delays or disruptions to supply chains.

Inflation expectations have now been on the rise for a few months, but stockmarkets have largely maintained their positive momentum and appear to be relatively unconcerned. Over the last week, sentiment was supported by the fact that rising expectation inflations were accompanied by rising expectations for economic growth. The same survey of business activity for the Eurozone demonstrated that service sector activity is already rebounding despite the remaining lockdowns, as reported output in services rose at its fastest pace for several years. The EU scored a rare pandemic victory with agreement for the creation of an EU Digital Covid Certificate, which will store data on vaccinations and tests. If widely adopted, it will allow vaccinated EU citizens to travel freely within the bloc as early as June, providing a boost to the leisure sector. In the UK, data on business activity, retail sales and consumer confidence all beat expectations, pointing to a strengthening in economic growth expectations.

Central bankers, meanwhile, have been able to keep the lid on fears of a change in monetary policy and, consequently, bond yields. European Central Bank officials last week renewed and reaffirmed their ultra-supportive policy stance: the bank’s chief economist dismissed the threat of a sustained increase in inflation as economic activity rebounds, while ECB President Lagarde said that it is "far too early, and actually unnecessary” to debate inflation as a long-term issue. The ECB has backed up these comments by recently increasing its purchase of bonds to a monthly run rate of EUR80 billion.

In the US, however, some Federal Reserve officials were unable to contain their discomfort with inflationary pressures, as revealed by last week’s publication of the minutes to their most recent meeting. In the press conference following the most recent meeting, Chair Powell had said that it was premature to start talking about reducing asset purchases. However, the minutes revealed that some officials were willing to debate whether the $120 billion a month in bond and mortgage purchases should be scaled back. To be sure, this was really a case of “talking about talking about” a slowing of asset purchases, but it did flatly contradict Chair Powell.

As a result, the grand guessing game goes on. The resurgence in economic growth caused by the end of lockdowns is creating pressures that normally require a tightening of monetary conditions and higher borrowing costs, but that is exactly what indebted governments can’t afford.

The so called 'streaming wars' is continuing to hot up with the news that Amazon.com Inc is nearing a deal to buy the Hollywood studio MGM Holdings for around $9 billion including debt. After Amazon's $13.7 billion purchase of Whole Foods in 2017, this deal would be Amazon's second-largest acquisition in history. MGM has a library of titles, including the James Bond franchise which it shares with the holding company owned by the Wilson/Broccoli family, and is best known for classics such as "Rocky", "Singin' in the Rain" and "The Pink Panther". While there are no guarantees an agreement will be ultimately reached, the potential acquisition of an iconic entertainment brand would be the most aggressive incursion yet by a tech giant into Hollywood. One that could heighten antitrust concerns at a time when Amazon is already facing multiple probes because of its size and power.

The American fracking industry is continuing a process of consolidation as US shale drillers Cabot Oil & Gas Corp. and Cimarex Energy Co. announced on Monday that they plan to merge in an all-stock deal. The combination brings together two firms extracting different commodities and operating in different regions. Cimarex is an operator in Texas, Oklahoma and New Mexico and focuses on oil; while Cabot is a natural-gas producer operating in the Northeastern US.

A joint venture between Industrial & Commerical Bank of China Ltd (ICBC) and Goldman Sachs Group Inc. has been approved by Chinese regulators, and comes as the country further opens up its financial markets to foreign banks. According to a filling by ICBC to the Hong Kong stock exchange, an ICBC unit will contribute 49% of the ventures funding and Goldman Sachs Asset Management will contribute the rest. It comes as other global financial firms have been moving to expand wealth management services in China.

Highlights

Annual consumer price inflation in the UK increased to 1.5% in April, from 0.7% in March, mainly reflecting a rebound in energy and clothing prices from March’s lockdown. Prices in the services sector are expected to gather pace as the year progresses, suggested further increases are in store.

Surveys of UK business activity for the first two weeks of May indicate that the rebound from the lockdowns is in full flow and business confidence is sky-high. However, the surveys suggest that inflation pressures are building: the survey’s index of output prices jumped to the highest level in its 23-year history.

It was a similar story in the Eurozone, where business activity rose well above expectations, particularly in the service sector. Businesses also reported sharply higher input price inflation, and an inability to meet orders as supply chains continued to deteriorate.

Calendar

The roller coaster in the US continues, with personal income likely to have plunged by 14% in April as the impetus from the latest round of stimulus cheques to households reverses. Personal income had rocketed by 21% when the cheques arrived in the previous month.

Weekly unemployment claims in the US are expected to continue their slow grind down, with 425,000 claims expected, compared with 444,000 last month. The semiconductor shortage may have slowed orders for aircraft and automobiles, when the US reports its durable goods order data for April.

Analysts will be watching consumer inflation expectations in the Eurozone for May, having risen in seven of the last eight monthly surveys.

This publication is intended to be Walker Crips Investment Management’s own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority and is a member of the London Stock Exchange. Registered office: Old Change House, 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.