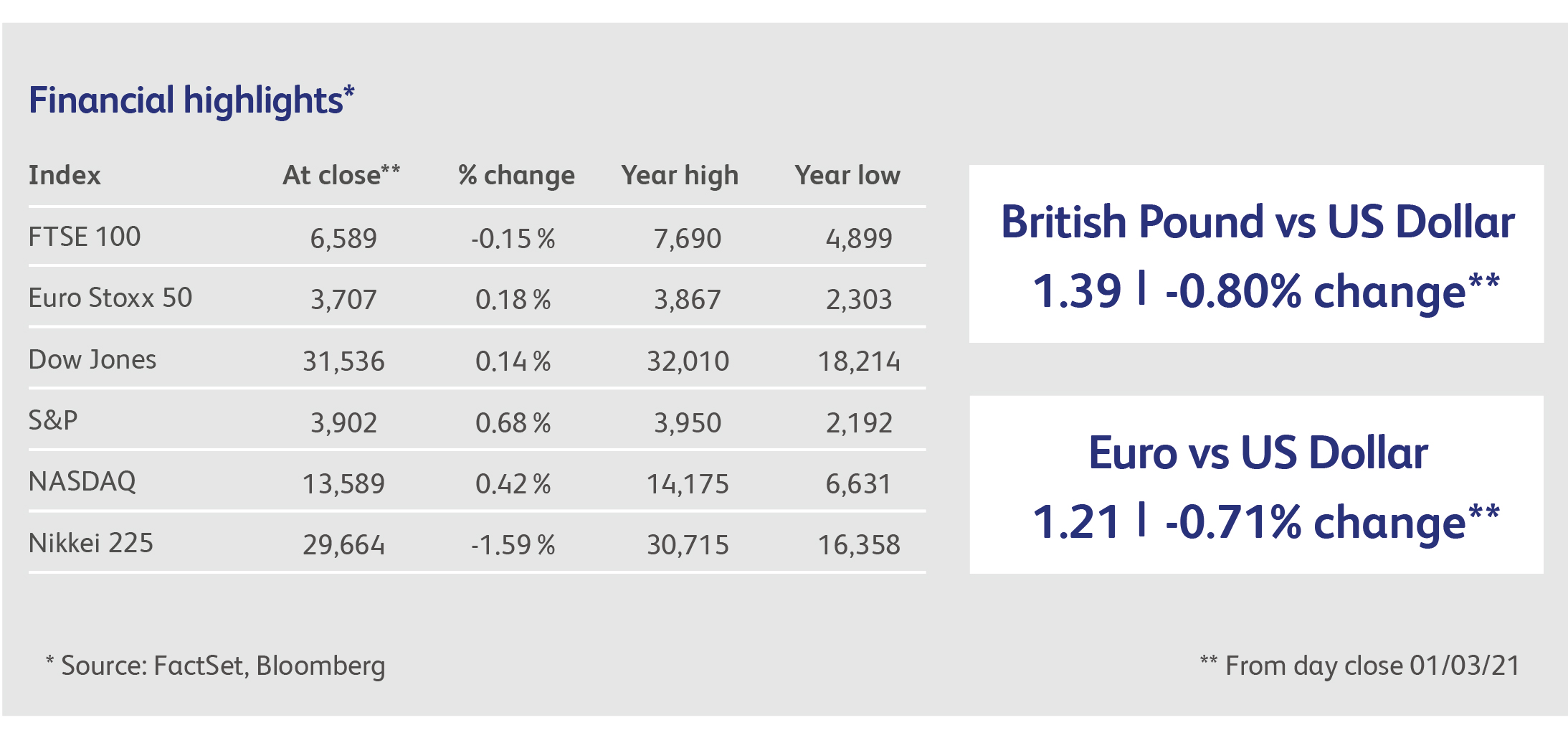

.jpg)

17 August 2021

The US inflation report for July passed without much market reaction, but that does not mean the threat of inflation has gone away. On the contrary, the report confirmed that US Consumer Price Inflation (CPI) is running at 5.4% a year, its second highest reading over the last 30 years. The difference this time was that economists actually got their forecasts right, having been far too optimistic over the previous few months. The details of the report showed a mix of risers and fallers: inflation in used car prices and airfares began to subside (but did not reverse), whereas the prices of food, restaurants and healthcare services are rising faster.

The UK inflation report for July, due out tomorrow, is expected to show a small decline compared with the previous month, falling to an annual rate of 2.3% from 2.5% in June. But this is just the calm before the storm, as inflation is then expected to surge to 4% by the end of the year, according to the Bank of England’s forecast. Consumers are going to have to put up with rising prices in food, due to extreme weather conditions (see Stock focus below), and in the prices of manufactured goods. The latter category includes electronic goods and cars, where supply has been constrained by shortages of semiconductors, but the problems go far wider than that.

One leading indicator of CPI is Producer Price Inflation (PPI), which measures changes in the prices of materials purchased (input prices) and factory gate prices (output prices). As one of the main sources of imported goods, China’s PPI is crucial, and it is currently running at 9% a year, the second-highest reading of the last 30 years. Euro Area PPI was 10.2% in June, including some hefty inflation in the German automobile industry. Goods manufacturers and wholesalers are not helped by the fact that shipping costs have gone through the roof. Since the beginning of the pandemic, the cost of transporting a shipping container from Shanghai to the big US port-hubs in Los Angeles has more than tripled, while the cost of shipping a container from Shanghai to Rotterdam has risen six-fold. The Baltic Dry Index, a London-based index of bulk shipping prices, has risen by 50% since the start of June and is up 800% from its pandemic lows. Prices were not helped by the blockage of the Suez Canal, which meant that the world’s stock of containers ended up in all the wrong places. More recently, cases of the delta variant in China have led to the shutdown of ports, including the world’s third-busiest at Ningbo-Zhoushan. Critical for consumer price inflation is whether firms can pass these increased costs onto customers.

Will inflation in manufactured goods now hand the baton over to service-sector inflation later? Given the importance of services in our modern economies, the labour market will be where the inflation battle will really be fought. And current wage growth is abnormally high. For example, UK average weekly earnings in the UK grew by 8.8% in June compared with the year before. However, this data is distorted by the effects of the furlough scheme, just as the US data is affected by enhanced unemployment benefits. With both the furlough scheme and the US benefits ending at the end of September, it will be several months before the employment picture becomes clear. Meanwhile, however, survey-based measures of employment growth, as well as of job vacancies, have rarely been stronger.

Airbnb joined Expedia and Booking Holdings in warning investors about the impact of the delta variant on its business for the third calendar quarter. The company expects bookings to fall below their level for the third quarter of 2019. Investors saw the bad news as good news: after opening 4% down, the shares rallied to end up on the day.

Disney, on the other hand, has seemingly avoided the delta variant completely – its theme park bookings for the third calendar quarter are running ahead of their second quarter levels. The company’s online TV business Disney+ also beat analysts’ expectations for subscriptions during the company’s last financial quarter. Investors saw the good news as no news: after opening up 4%, the shares drooped, managing a gain of less than 1%.

South Korea’s leading semiconductor manufacturers Samsung and Hynix were hit by what was described as “panic selling” last week, falling by 9% and 14% respectively. They were not helped by the South Korean won hitting a ten-month low. A spike in the delta variant and low vaccination rates in South Korea were supposedly to blame - the prime minister asked citizens to refrain from travel this weekend. The South Korean stock market’s Kospi index had its worst weekly performance since January, but is still up 11% for the year to date.

Tesla shares fell 4% after the US National Highway Traffic Safety Administration opened a formal investigation into Tesla’s Autopilot system. The probe covers an estimated 765,000 vehicles, and follows 11 crashes that resulted in 17 injuries and one death.

Wheat is the latest commodity price to surge to a multi-year high. Canada’s crop has been affected by heat and drought, following the hit to Russia’s crop caused by extreme winter weather. Higher breads, pasta, and breakfast cereal prices are certain.

Highlights

Calendar

UK Consumer Price Inflation is expected to have fallen to 2.1% in July, from 2.5% in June. Rising prices for food, electronic goods, transportation and accommodation costs are likely to have been offset by falling clothes prices. In any case, inflation is expected to pick up again before the end of the year.

This publication is intended to be Walker Crips Investment Management’s own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority and is a member of the London Stock Exchange. Registered office: Old Change House, 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.