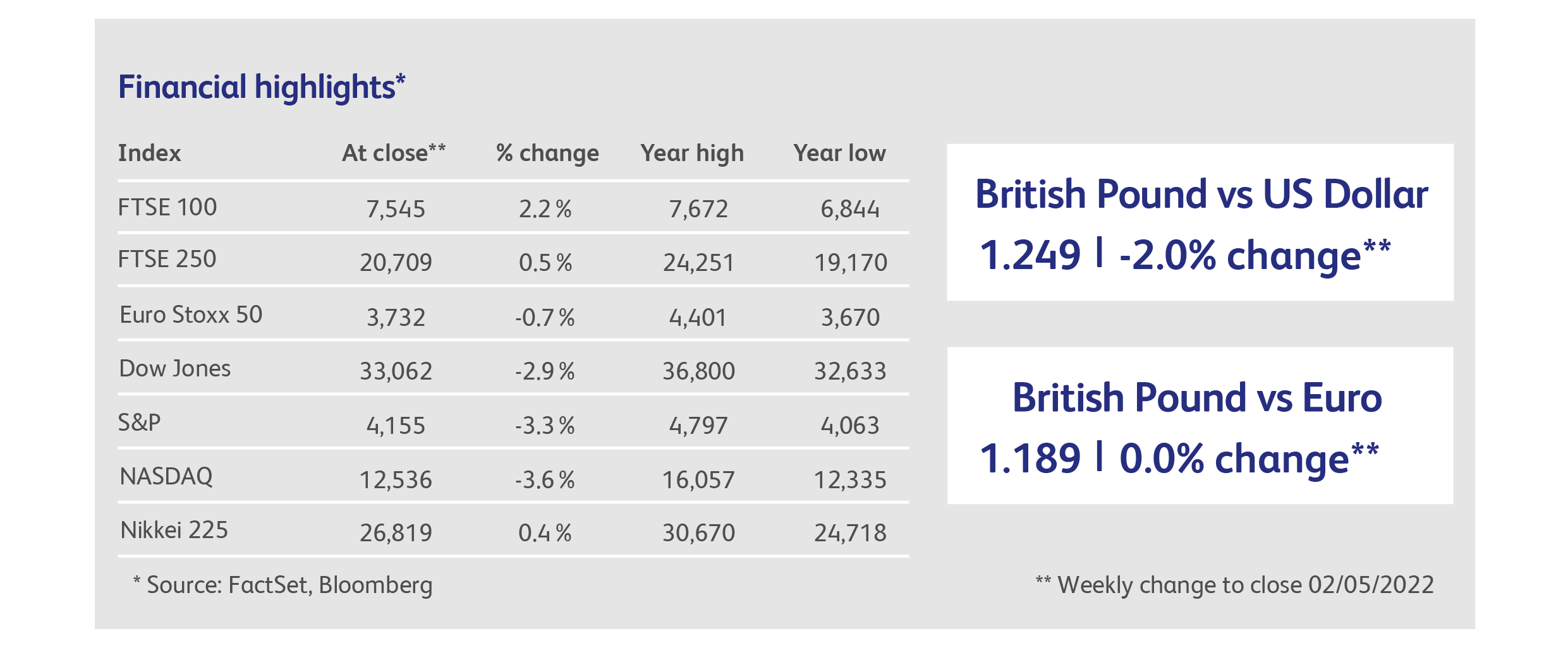

3 May 2022

Volatility in stock markets was back to its post-pandemic peak last week, with the mighty S&P 500, the world’s largest stock market index by value, falling by 2.8% on Tuesday, only to rise by 2.5% on Thursday, before selling off 3.6% on Friday. So much of the value of the S&P 500 is now concentrated in a few technology behemoths that their fate determines its fate. Thursday’s rebound had much to do with unexpectedly strong results from Meta Platforms (formerly Facebook) amongst others, and Friday’s sell-off appeared to have been triggered by disappointing results from Alphabet and Amazon, combined perhaps with the negative outlook expressed by Apple’s management. However, these problems were mainly related to the pandemic’s distortion of supply and demand. Alphabet reported a deterioration in demand from customers in Europe, but this should be seen in the context of a quarter in which Alphabet’s revenues still grew at a 20% rate.

In fact, demand for companies’ products and services generally is so far holding up well, as are the expectations for company profits. Results for the first calendar quarter of the companies comprising the S&P 500 show that healthy profit margins have been maintained, revenues have grown at a double-digit pace and profits are comfortably above last year’s levels. Looking forwards, profit forecasts for 2022 for constituents of the S&P 500 have actually risen by 5% since the start of the year. The root cause of the market’s current woes is, therefore, not so easy to identify.

Admittedly, inflation and its consequences, including higher interest rates, can shoulder a lot of the blame. As the cost-of-living rises, more income is spent on the basics and less is available for other uses that might grow the economy. This has led to reductions in economic growth expectations across the globe. However, no major economies are yet predicted to fall into recession. In fact post-pandemic growth is still expected to rebound at a fairly rapid clip, even after taking into account the effects of inflation. Moreover, the pandemic was accompanied by a vast accumulation of wealth amongst consumers that benefited from government stimulus and enforced saving. In fact, for many consumers the impact of inflation is dwarfed by this wealth-accumulation. This suggests that there might be other, less obvious factors at work.

One less visible but important factor is the role of financial securities as collateral for loans, which are often used to buy other securities. Margin debt of this kind exploded during the pandemic, along with just about every other kind of speculation, adding almost half a trillion dollars of buying power at its peak in the US alone. This has yet to fully unwind. Bonds are also popular as collateral for loans to leveraged players, typically hedge funds, and their decline in value will have restricted the ability of hedge funds to hold positions funded using loans.

Ultimately, of course, prices are determined by supply and demand and, in this respect, there is reason to be concerned. Whether it was a direct result of government stimulus, enforced saving or just pure speculation, the pandemic was accompanied by the biggest inflow of investors’ savings into US equity funds in history. Over $1 trillion flew into US equities via open-ended funds during the pandemic, more than in the whole of the preceding decade. Granted, this is not the only source of demand for equities but it is a substantial number: if that money were to shrink back to normal levels of investment, it could create a serious headwind for stock prices.

Alphabet, parent of Google, announced a 20% increase in revenue for the first calendar quarter, to $56 billion, but it was not enough to please investors and the stock fell 3% on the news. YouTube’s advertising revenues were particularly underwhelming, and the company highlighted a slowdown in advertising expenditure in Europe. Even the announcement of a $70 billion share buyback program could not arrest the decline in the share price, which has fallen 17% in the last month.

Amazon’s share price had its worst day since 2006 and the company’s value declined by $206 billion after reporting a loss of $4 billion for the first quarter; its first quarterly loss in seven years. The company’s binge on hiring and warehouse building during the pandemic now looks flat-footed given the return to normal after the lockdowns. Management admitted it currently has too many warehouses and workers, but reported that demand remains strong, with revenues growing by 7% in the quarter.

Pandemic icon Robinhood.com reported a fall in revenues of 43% for the quarter, as retail day-traders in the US became more cautious with their portfolios, trading less frequently and in smaller amounts. The company reported that cryptocurrency revenues were particularly hard-hit. Robinhood.com’s share price is down 86% from its brief, post-IPO peak of August last year.

In one of its last earnings announcements as a public company, Twitter reported slower growth despite a 16% increase in daily active users to 229 million. The company reported that an error had causes it to over-report the numbers of daily users over the past three years.

US oil giants Exxon and Chevron sent a strong message to investors about their investment prospects when they followed strong first quarter results by doubling their share buyback programmes. Between the two companies, buybacks will now exceed capital expenditure for the first time since 2008.

This publication is intended to be Walker Crips Investment Management’s own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority and is a member of the London Stock Exchange. Registered office: Old Change House, 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.