5 July 2022

It was a week in which market behaviour began to shift away from fear of interest rates rises towards fear of recession. This was most evident in a recovery in government bond markets where, at the short maturities that most clearly reflect the expected path of interest rates, a dramatic shift could be seen. In the blink of an eye, seemingly, investors have shifted from being convinced that the US Federal Reserve will do multiple rate-rises, to being convinced that softening global growth will soon translate into weaker inflation, putting the Fed on hold. Markets are even now pricing in 0.75% in rate cuts in 2023. Bond values were driven upwards by a series of poor economic data, including more declines in consumer confidence around the developed world and an American survey of manufacturers that indicated a rapid decline in activity.

The American experience was repeated in Europe, where short-term German bonds registered upward moves seen only once a decade after German inflation fell for the first time since January. A closer look at the details, however, suggested that the fall was mostly due to one-off government measures, including a cut in fuel duty and the introduction of heavily discounted rail fares. Inflation in the Eurozone more broadly rose to 8.6% in June, which was above expectations, but even this did not dampen the enthusiasm of bond market analysts, who pointed to a decline in so-called “core” inflation, which excludes more volatile components. To complete the picture, gilts surged after a business activity survey showed that Britain’s manufacturing sector is also running out of steam.

Unfortunately, the waning of interest rate expectations did not boost stock markets, which became caught up in the fear of recession and its impact on corporate profits. It did not help that profit warnings are spreading from the retailers to other industry sectors and, in each case, fear of a slowdown in consumer spending is accompanied by fear that companies are holding too much stock just at the wrong time. This has the makings of a boom-to-bust cycle, the like of which has not been seen since the 1970s.

Given that economic data is published with a sizeable time-lag, the coming weeks are unlikely to assuage fears of impending recession. China did provide some respite, however, with indications that the authorities are inching away from the “Covid Zero” policy that has forestalled China’s recovery from the pandemic. Mandatory quarantine periods for travellers from abroad were halved, which prompted strong gains in Chinese travel and tourism stocks. Domestic travel restrictions were also eased, and business activity surveys showed that China’s economy is returning to health after the lockdowns of the last few months. Furthermore, in a widely-telegraphed move, the American government may also be about to roll back some of former president Trump’s tariffs. Together with the recent expressions of support from the domestic authorities, the hope is that China can mount an economic recovery large enough to move the needle for the entire global economy.

The semi-conductor sector was the latest industry to inflame fears of a recession after a very poor sales report and a profit warning from Micron Technology, the largest US manufacturer. The chip drought from the pandemic years has morphed into a chip glut, at the same time as customers are beginning to reduce demand. Shares of semi-conductor makers around the world fell by 4-5%. Given their ubiquity, semi-conductors are regarded as a barometer for global demand across a range of industries.

Analysts at investment bank Morgan Stanley took the unusual step of placing a lower-bound valuation of zero on shares in cruise-line operator Carnival Corp, prompting the shares to fall 16%. This is despite the company having enjoyed a 10% rally in the previous week after it reported a surprisingly strong customer pipeline. Having accumulated huge debts during the pandemic, the company is now thought to be at risk from cancellations and weaker bookings.

Airbus shares rose 4% after the company reported one of its largest-ever orders for 292 aircraft, worth $37 billion from four different Chinese airlines. Airbus’ local assembly line in China may have helped secure the business, while political tension between America and China won’t have helped Boeing’s chances. However, Boeing’s shares also rose on the news, perhaps encouraged by its promise for market growth.

The entire spectrum of commodities has reversed their spectacular performance of earlier in the year and are slumping. Base metals are leading the downtrend, with Nickel having fallen by over 50% from its high in March. Agricultural commodities have fared a bit better, having fallen by 10-20% from their highs in most cases, but Cotton is an outlier at down 37%. Among precious metals Gold has held up best, whereas Silver, Platinum and Palladium are all down over 20% from their recent highs.

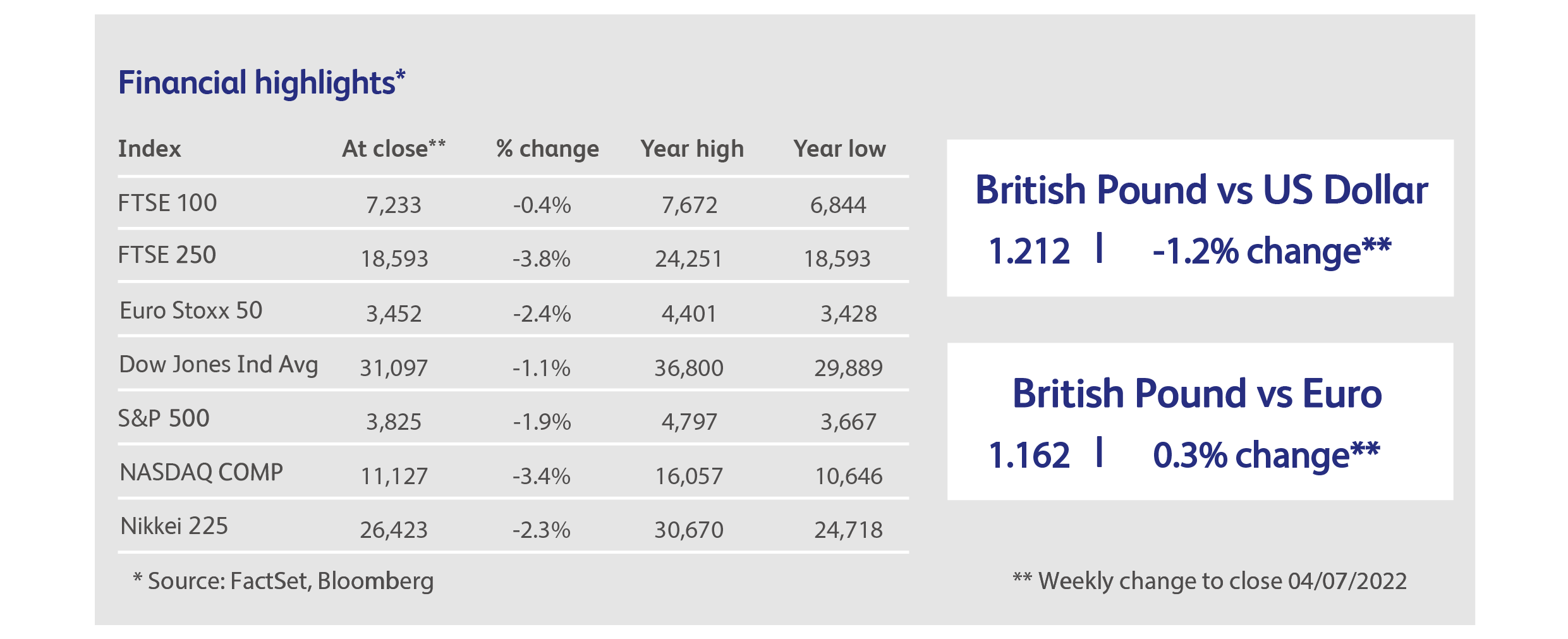

Highlights

Calendar

This publication is intended to be Walker Crips Investment Management’s own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority and is a member of the London Stock Exchange. Registered office: Old Change House, 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.