3 March 2026

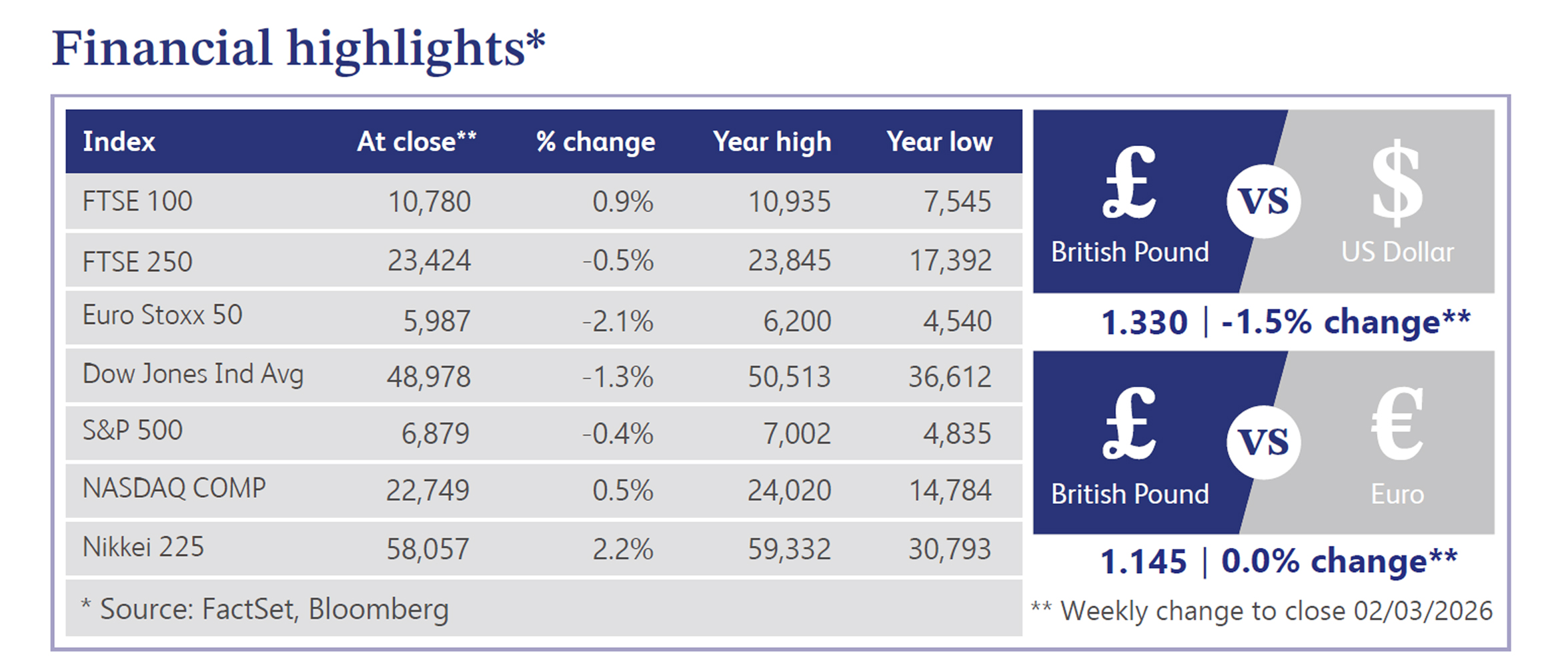

Last week, Bank of England (“BoE”) Monetary Policy Committee (“MPC”) member Alan Taylor noted that inflation appears to be heading towards normalisation, paving the way for a potential dovish shift. Governor Bailey's belief that a fall in inflation is "baked in" has led markets to price in an 80% chance of a 25-basis-point interest rate cut on the 19th March. The UK labour market is weakening, with job advertisements at a five-year low and youth unemployment, although above the EU average, worsened by nearly a million young Britons not in education, employment or training. Businesses and consumers fear job losses, as shown by a dip in the GfK Consumer Confidence measure, exacerbated by rising payroll taxes and minimum wage increases. Political uncertainty persists after PM Starmer's Labour Party lost the Gorton and Denton by-election to the Green Party, with Reform UK in second place.

In equities, the FTSE 100 index finished the week moving up to 10,780, bringing its year-to-date gain of 8.33%. Meanwhile, Chancellor Rachel Reeves is preparing to deliver a subdued Spring Statement today, aiming to end the cycle of policy speculation and reassure businesses. This follows positive news from the National Audit Office, which showed HM Revenue & Customs collected an extra £16 billion from the biggest firms last year through an intensified, "hands-on" compliance approach. Despite this fiscal headroom, Reeves is expected to announce an uneventful update with no major new policies in order to maintain market stability. UK officials are lobbying the United States (“US”) to cap proposed universal tariffs on British exports at 10%, after the US raised tariffs to 15%, adding up to £3 billion in costs for exporters, as officials seek to protect the transatlantic Economic Prosperity Deal. In currency markets, sterling weakened against the dollar to 1.330.

Across the Atlantic, economic data was mixed: January's core Producer Price Index ("PPI") was hotter than expected, a four-year high on a month-on-month basis, but February consumer confidence data rose due to better labour market perceptions, whilst jobless claims held steady. Meanwhile, major US equity indices declined: the Dow Jones Industrial Average fell 1.3% and the S&P 500 dropped 0.4%. Research from Citi warning of Artificial Intelligence (“AI”)-driven white-collar job losses, weaker consumption and private credit stress sparked an early week $220bn software sell-off. Pressuring AI-linked names such as IBM (-6.59%) and NVIDIA (-6.8%), despite strong earnings amid positioning and growing AI-fatigue concerns. Treasuries were firmer, steepening the yield curve. The US Dollar Index rose 0.6%, and Gold was up 3.3%. WTI crude oil was initially up 0.8% Friday amid US-Iran tensions. Over the weekend, the situation escalated into war following US and Israeli strikes on Iran, killing Supreme Leader Ayatollah Ali Khamenei. This major geopolitical conflict and ensuing regional instability are expected to significantly raise global crude oil prices, with WTI futures jumping 13% to $82 per barrel.

The UK housing market experienced an increase in activity early this year, with property listings rising 6% year on year. This increased supply is expected to keep house price growth in check throughout 2026.

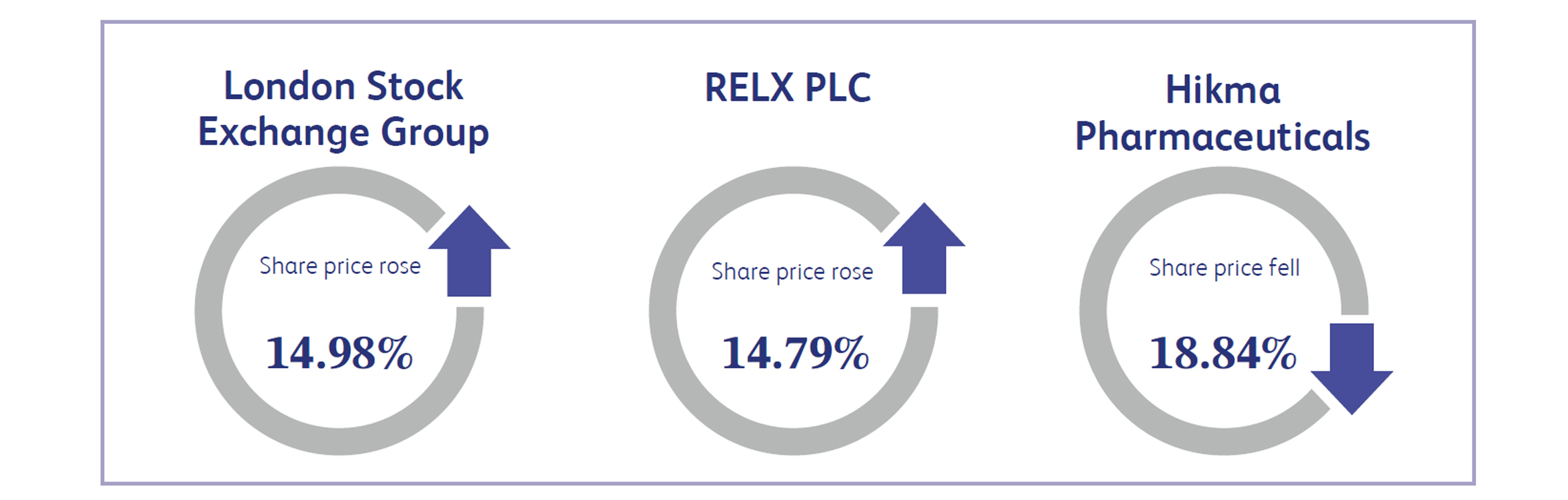

London Stock Exchange Group, the British-based stock exchange and financial data provider, surged 14.98% as investors aggressively bought back into the stock following a recent technology-driven sell-off. The sharp rebound, which highlights the market's renewed appreciation for the firm's highly rated data analytics businesses, underscores the underlying resilience and reliable earnings power still present within UK blue-chip financial firms despite broader anxieties over AI disruption. This upward momentum further validates the appeal of high-quality market leaders, as investors capitalise on attractive valuations to back proven, globally diversified operators.

RELX PLC, the British multinational information and analytics company, rose 14.79% after major UK asset managers bolstered their positions in the stock, capitalising on an attractive valuation following a recent sector-wide tech sell-off. The substantial gain, which highlights the firm's robust economic fundamentals and medium-term growth potential, underscores the underlying resilience and reliable cash generation still present within UK software stalwarts despite broader market fears over artificial intelligence. This positive assessment from institutional investors signals confidence in the company's strategic direction and its ability to maintain a competitive edge.

Hikma Pharmaceuticals, the British multinational generic pharmaceutical company, fell 18.84% after experiencing a significant negative market reaction, raising concerns regarding its near-term earnings outlook. This was following the company's guidance to group revenue growth of 2-4%, below consensus expectations of 5.6%. The sharp decline, which highlighted fears that its core business is moving into a period of diminishing returns amid intensifying pricing pressures and macroeconomic headwinds, underscores the underlying vulnerability still present in United Kingdom healthcare stocks despite the broader resilience of the London market.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.