12 May 2026

Last week, Bank of England (BoE) Governor Andrew Bailey warned that insurers and pension funds have become dangerously intertwined with the private credit market. This concern follows a major hit to the financial sector earlier this year. While the Middle East conflict continues to drive energy prices higher, the Monetary Policy Committee (MPC) expects an economic slowdown. Geopolitical uncertainty has fuelled worries about rising food prices and energy bills, which impact roughly 80% of people. Consequently, officials are likely to discount upcoming growth figures as seasonal strength fades, preferring to monitor long-term stability rather than reacting solely to temporary economic growth data points.

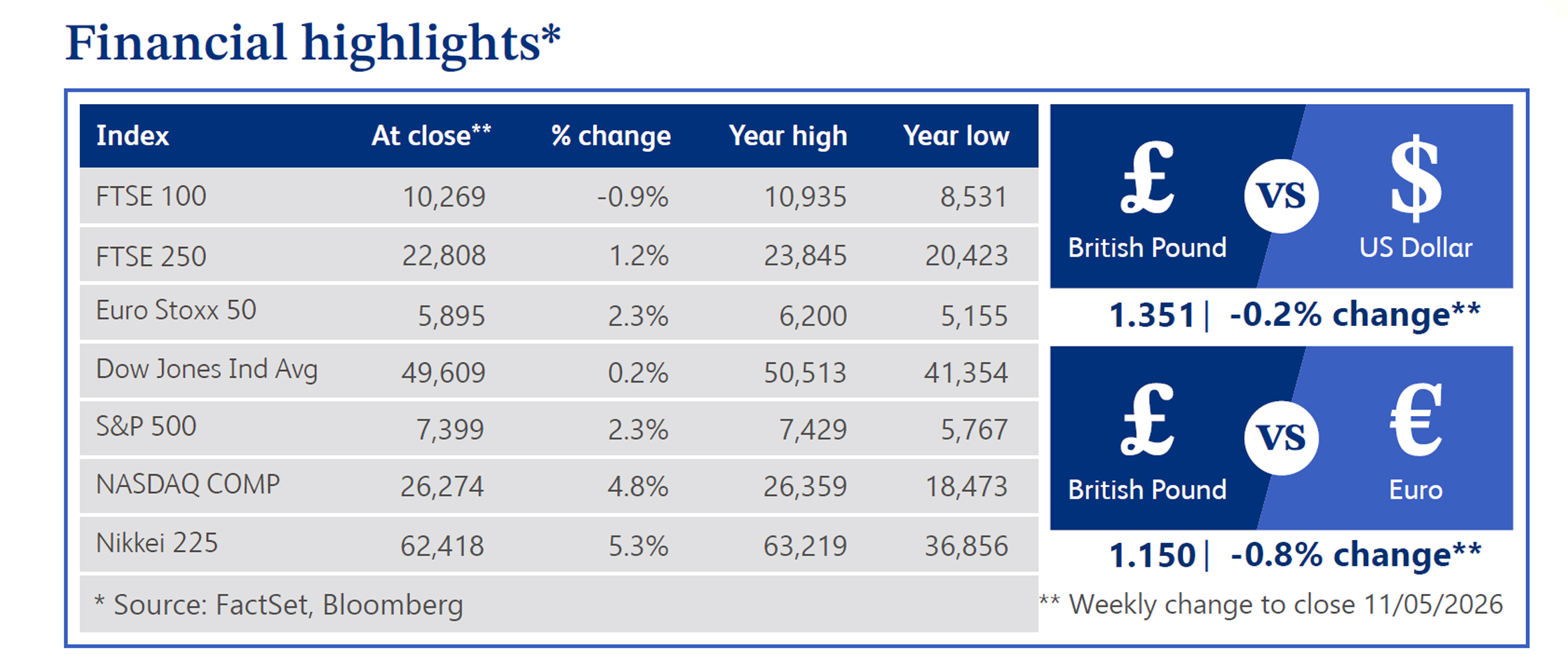

Elsewhere, UK government bonds came under pressure as markets reopened following Monday’s bank holiday. Benchmark 10-year Gilt yields reached an eighteen-year high of 5.05% on Tuesday as investors responded to surging crude oil prices. Markets now anticipate three additional BoE rate hikes by the end of the year. In equities, the FTSE 100 index finished the week relatively flat. This trend masked a significant underlying trend: selective UK investors continued their pattern of committing new capital primarily to US and global index-tracking funds. This preference came at the expense of traditional domestic UK active equity funds, which continued to see muted inflows or even outflows as investors pursued broader diversification and exposure to international markets, particularly the strong performance seen in the United States.

Across the Atlantic, macroeconomic data remained supportive of risk sentiment as non-farm payrolls reached 115,000, well ahead of the 65,000 consensus. In equities, the S&P (Standard and Poor’s) 500 index finished the week at record highs with a 2.33% advance while the Nasdaq Composite climbed 4.51%, marking a sixth weekly gain for both. Technology stocks led the rally, driven by enthusiasm surrounding Artificial Intelligence (AI) and semiconductor performance following earnings results. United States (US) Treasury prices were little changed to firmer despite hawkish Federal Reserve (Fed) takeaways that prompted markets to price in additional rate hikes.

Meanwhile, the US Dollar Index (DXY) weakened by 0.3% as gold prices increased 1.9%. Geopolitical developments remained central to sentiment as diplomatic negotiations over the Iran conflict progressed, with a proposed memorandum of understanding involving Trump envoys. Despite initial escalations and continued tensions, the anticipated path toward a resolution, or at least a de-escalation of the conflict, significantly pressured energy markets. This anticipation sent West Texas Intermediate (WTI) crude oil down sharply, closing 6.4% lower on the day, as traders priced in a potential return of Iranian supply or a reduction in regional risk premium.

Despite economic volatility, UK house prices were broadly stable in April, with the Halifax reporting a marginal 0.1% monthly dip and 0.4% annual growth, supported by robust wage increases aiding affordability. However, rising mortgage rates (now over 5.1%) are increasing pressure. This is reflected in the construction sector, where RICS noted a decline in private housing workloads to a net balance of -19% due to escalating costs.

Endeavour Mining, which operates a portfolio of high-quality gold mines across West Africa, shares rose 11.61% this week. After releasing its Q1 2026 results on 30th April, which showed record free cashflow at $613 million, the company benefited from a positive reaction from investors. Endeavour Mining also benefited from the broader rally in precious metals, with gold prices increasing 1.9% as investors sought safe-haven assets amid ongoing Middle East tensions. This upward momentum in bullion provided a significant tailwind for the mining sector, supporting valuations for producers with large-scale operations. Specifically, robust prices for gold and silver bolstered the financial outlook for companies focused on precious metals, enabling them to generate stronger cash flows. This positive sentiment is further underpinned by the sustained confidence investors place in the sector's major players.

JD Sports Fashion, which operates a global network of retail stores specialising in branded sports fashion and outdoor apparel, performed well, rising 11.56% last week after releasing its FY26 results on 7th May. Despite a drop in Profit before Tax due to exceptional items of £852 million, the Free Cash Flow increased by £123 million to £462 million. The gains reflect broader resilience in leisure spending, which has remained surprisingly robust despite inflationary pressures on households. While some retail sectors faced headwinds from rising energy costs, JD Sports benefited from its strong international footprint and demand for premium footwear. Analysts believe the company’s strategic expansion into North American markets supports sustained long-term growth.

RELX, which provides information-based analytics and decision tools for professionals and businesses, shares fell 8.82% during the period. The decline comes as investors rotated out of high valuation analytics and technology sectors following recent strength in the market. Although the company remains a leader in scientific publishing, concerns regarding the potential for Artificial Intelligence (AI) disruption in professional services weighed on sentiment. The sell-off was further exacerbated by a shift toward cyclical stocks as macro data suggested resilience.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.