13 July 2021

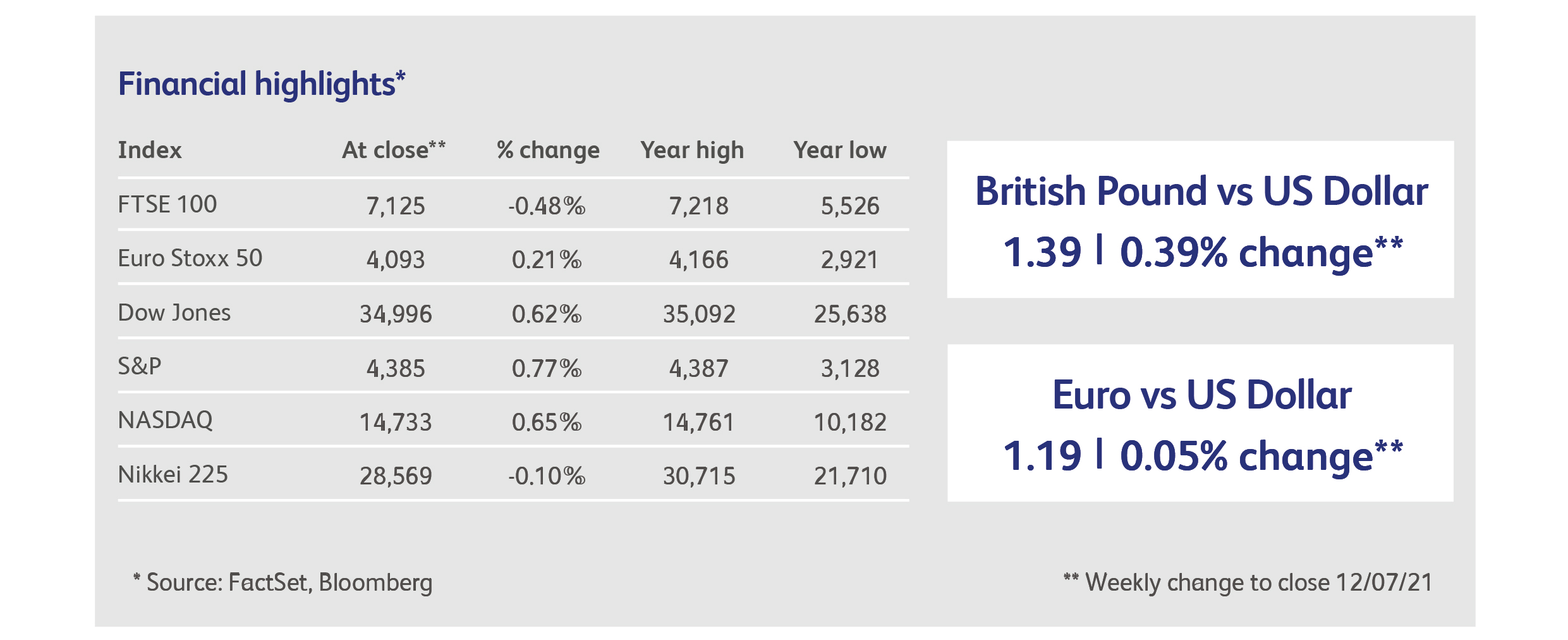

Global markets were mixed over the past week as domestic and European bourses saw little change. US indices moved to fresh highs despite the S&P 500 breaking its longest winning streak since August after traders returned from the Independence Day public holiday. Investors remained focused on the sharp decline in long-term rates, which initially buoyed equity markets but led to concerns about stalling global growth as the week progressed. No one specific factor was to blame, but commentators pointed to a retreat in the longstanding reflation trade amid warnings of peak growth. Sentiment improved as the weekend approached thanks to raised expectations for solid second-quarter earnings reports and positive news about the Pfizer vaccine.

Previously, Japanese share prices fell after a state of emergency was declared to curb the spread of the highly contagious delta coronavirus variant. A ban on spectators at this summer’s Olympics in Tokyo will also dent Japan’s broader economy. In contrast, there is little or no appetite for such restrictions in the US and most of Europe, with governments encouraging high levels of vaccine take-up instead, in spite of rising case numbers.

Around 70% of the UK population has now received at least one jab, and the UK Government recently cut the gap between doses from 12 weeks to eight for all adults. The programme’s success has been a significant factor in lifting the remaining lockdown restrictions on 19 July. After that date, there will be no legal obligation to wear face masks or socially distance, and workers will not be required to work from home where possible. Even so, the public are being asked to exercise caution and the Health Secretary Sajid Javid has said people should still wear face coverings unless they're exempt in crowded indoor settings. Moreover, it is hoped that ‘Freedom Day’ will provide a much-needed boost to theatres, venues and events which have been forced to close for over a year. During this time, other consumer-facing services such as retail and hospitality have almost returned to full health, and growth in these areas helped the UK economy grow for the fourth consecutive month in May. Data from the Office of National Statistics suggest that the UK economy is now just 3.1% below its pre-pandemic February 2020 levels.

However, the pace of recovery is beginning to slow. Analysts had expected growth of 1.5% in May but the increase was tempered by slowdowns in car production and building work caused by shortages of computer chips and commodities such as timber and steel. The trend is not limited to home soil either; the chip shortage has affected manufacturers and automakers in Germany, and gauges of optimism in the US have fallen back to levels last seen in February.

Global central banks remain reluctant to tighten monetary policy under such conditions, which means rising inflation remains a potential threat. Oil prices continue to increase, and OPEC+ abandoned its latest meeting without a deal due to a rift between Saudi Arabia and the UAE. Supply could remain at current levels despite the rising demand for fossil fuels. Many believe that the recent spike in inflation will prove temporary, but consumer price figures out later this week may provide more clues in this respect.

Following Sir Richard Branson’s successful foray into suborbital space on Sunday, New York listed Virgin Galactic Holdings announced its intention to raise up to $500m via the sale of stock. The cash is intended to help boost working capital and assist with capital expenditures as the company looks to ramp up its manufacturing capabilities and develop its fleet of spacecraft ready. Their intention is to begin commercial flights to suborbital space in 2022 - they have approximately 600 customers waiting to spend c. $200,000-$250,000 each on the 2-3 hour journey which will include 4-5 minutes of weightlessness.

The Rothermere family are considering taking the Daily Mail & General Trust (DMGT) private via its vehicle Rothermere Continuation Ltd, which already owns c. 30% of the company’s shares. Lord Rothermere owns all of the DMGT’s voting shares, so any bid for the company by the family will be seen as a formality, as long as DMGT can dispose of its insurance risk division and also its stake in the online used car sales portal Cazoo (likely via the listing of its shares on the New York Stock Exchange).

The Chinese technology company Tencent Holdings came under fire from it’s home country’s antitrust regulator, which is ordering its Music Entertainment division to give up its exclusive rights deals with music labels such as Universal, Sony and Warner. This move is seen as China’s latest attempt to clip the wings of its major technology companies and pave the way for greater competition from smaller rivals. In addition to the order to give up its exclusive deals, the regulator also imposed a fine of c. $77,000 USD. Whilst the sum may be immaterial, it serves as a warning that the regulator’s radar is firmly switched on.

Highlights

Minutes from the Federal Open Market Committee’s June meeting revealed that policymakers believe it may soon be appropriate to tighten monetary policy, but that most committee members are hesitant to begin tapering the Fed’s asset purchases immediately preferring instead to wait for more evidence of a robust economic recovery.

ECB’s Governing Council approved its new monetary policy strategy which included the adoption of a symmetric 2% inflation target over medium term whereby both negative and positive deviations from the target are equally undesirable. The announcement also highlighted an action plan that will include climate change considerations in its decisions.

Calendar

US Inflation is expected to remain close to May’s level of 5% which was the highest reading since August 2008. UK CPI is expected to increase to 2.3%.

The Chinese economy advanced 18.3% year-on-year in the first quarter of 2021. Forecasts for the second quarter reading currently stand at 8%.

This publication is intended to be Walker Crips Investment Management’s own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority and is a member of the London Stock Exchange. Registered office: Old Change House, 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.